TWINO review 2025

Read this TWINO review to learn if the platform is for you.

TWINO

Pros

Cons

TWINO review summary:

After several years on the market, TWINO has proven to be a serious P2P platform. They offer competitive rates to their investors. At the same time, TWINO has also created a profitable business, which means that they have a better foundation than many unprofitable alternatives. Investing with the platform is made easy with auto-invest portfolios and safe with buyback/payment guarantees.

It’s 100% free to open an account

Introduction to our TWINO review

TWINO is one of Europe’s pioneering P2P lending platforms. This TWINO review explores its main features, considers its safety for investors, and shares tips for those thinking of investing. Please note this is an opinion-based review, not investment advice.

Learn about the following in our TWINO review:

- What is TWINO?

- What is the return on TWINO?

- Is it safe to invest on TWINO?

- Who can invest on TWINO?

- How to invest on TWINO?

- How to withdraw money from TWINO?

- What are the best TWINO alternatives?

- Conclusion of our TWINO review

What is TWINO?

TWINO is a Latvian peer-to-peer lending platform launched in 2015. It offers advertised returns of up to 12% by providing access to short-term consumer loans, primarily from Poland, as well as real estate investments within Latvia.

TWINO works by allowing loan originators to pre-fund the loans, which are then listed on the platform. Investors can choose which loans or projects to fund, typically receiving monthly interest until the loan matures. The minimum investment is just €1, making it accessible to a wide range of investors.

The platform has attracted over 63,000 investors who have funded more than €1.1 billion worth of loans since the platform’s launch.

AS TWINO Investments is regulated as an investment brokerage firm supervised by the Central Bank of Latvia, operating under license number 06.06.08.720/536.

TWINO statistics:

| Launched: | 2015 |

| Investors: | 63,000 + |

| Interest rate: | 8 – 12 % |

| Loan period: | 1 – 60 months |

| Loan type: | Consumer |

| Loans funded: | € 1,100,000,000 + |

| Min. investment: | € 1 |

| Max. investment: | Unlimited |

TWINO Trustpilot rating

TWINO has received a TrustScore of 2.4/5 based on 74 reviews on Trustpilot. While some investors commend its user-friendly interface, secondary market liquidity, and the potential for steady returns, others criticize the platform for weak communication, questionable buyback guarantee enforcement, and long delays or suspensions in principal repayments. Despite these concerns, TWINO’s licensing progress and efforts at transparency offer some reassurance for users seeking to diversify their p2p lending portfolio.

What is the return on TWINO?

TWINO’s average annual investment return is 12%. Compared to other P2P platforms, this figure places TWINO near the middle of the spectrum, where some providers offer returns as high as 15–16%. High returns typically indicate a higher level of risk, and TWINO falls into the moderate-to-high risk category given its double-digit returns.

The interest rates on TWINO ranges from 10% to 13%, creating a window where returns might vary depending on factors such as loan type, repayment schedules, and borrower risk. While these rates are relatively competitive, the stability of returns can fluctuate if loan repayments are delayed or if market conditions change.

TWINO fees:

- Deposit fee: No

- Investment fee: No

- Inactivity fee: No

- Selling fee: No

- Withdrawal fee: No

TWINO does not charge any fees to investors for using the platform. Opening an account, investing, and withdrawing funds are all free of charge, making it simple for investors to understand their real returns without needing to account for additional fees.

Instead of passing costs onto investors, TWINO earns its revenue by charging commissions to the loan originators that list their loans on the platform.

Being entirely free for investors, TWINO stands out from platforms like Mintos, which incorporate various charges, such as a secondary market selling fee and currency exchange fees.

Special welcome bonus

Readers of this TWINO review are eligible for a €20 cashback bonus for the first investment. To unlock this special offer, new investors must sign up using the button below and invest at least €100. No TWINO promo code is required.

How does TWINO handle taxes?

TWINO is legally required to withhold taxes on interest income from loans on its platform. This can make handling your taxes more complex than on platforms such as PeerBerry, Robocash, or Esketit, which do not withhold taxes.

The standard withholding tax rate on TWINO is 5% for EU/EEA tax residents and 20% for all others, including Latvian tax residents. Investors from Lithuania can reduce their tax rate to 0% by providing a valid tax residency certificate.

Tax report

TWINO provides a tax report to help you declare your earnings to local authorities. You can easily download your income statement from your dashboard on your investment account under “Reports”.

Is it safe to invest on TWINO?

TWINO is not considered one of the safest P2P lending platforms in Europe. While most loans on the platform are covered by a buyback guarantee, the effectiveness of this guarantee has been critiqued by some investors on Trustpilot, suggesting that its reliability might not always meet expectations.

Licensed and regulated platform

AS TWINO Investments is regulated as an investment brokerage firm supervised by the Central Bank of Latvia, operating under license number 06.06.08.720/536. This indicates that it is a legitimate company and not a scam.

Profitability

Compared to a lot of other P2P lending platforms, TWINO is very open about its financials. As an example, they post all their financial reports on the website, which makes them easy to access if the company has solid financials.

Insolvency protection

TWINO participates in the national investor compensation scheme of the Republic of Latvia, aligned with the EU Directive 97/9/EC. If the platform becomes insolvent and cannot provide investment services, retail investors are eligible for compensation covering 90% of any irreversible loss, up to a maximum of €20,000.

TWINO is required to keep investor funds separate from its own account, which means that in the event of insolvency, investor funds are safeguarded and cannot be accessed by creditors to settle TWINO’s debts.

TWINO buyback guarantee

On TWINO, most loans are covered by a 60-day buyback guarantee. This means that if a borrower is more than 60 days late with repayments, the loan originator automatically repurchases the loan from the investor along with accrued interest.

The TWINO buyback guarantee has a duration of 60 days, which is the industry standard. This is longer compared to Robocash and Loanch, which offer the shortest buyback duration on the market at 30 days.

Investors should keep in mind that the reliability of the TWINO buyback obligation depends on the financial stability of the loan originators. If the loan originators are unable to buy back the loans, the buyback guarantee becomes worthless.

TWINO payment guarantee

On some of the loans, TWINO has a payment guarantee instead of a buyback guarantee. Contrary to the buyback guarantee, here you do not have to wait 60 days to get the interest on your loans. In the event of a payment guarantee loan being defaulted, you will receive money from TWINO according to the original payment plan.

Please note that not all loans are covered by the payment guarantee. The covered loans are marked in the loan listing on their website.

Two-factor authentication

TWINO offers two-factor authentication (2FA) to strengthen account security. This feature works with the Google Authenticator app, generating unique, time-based passcodes that protect investor funds from unauthorized access. Since hackers have targeted P2P lending platforms in the past, enabling 2FA is strongly recommended.

Who can invest on TWINO?

TWINO accepts investors from European Economic Area countries. Both individuals and companies can use the platform.

To invest on the platform, you must also be at least 18 years old, and be able to prove your identity.

If you meet these requirements, you can register at TWINO using the following steps:

- Create an account

- Add money to your account

- Start investing

- Earn interest

Please note that when you add money to your account, all future operations under your account will be made in the currency of your first deposit. If your first deposit is GBP, all future activities on your account will be dealt with in GBP. Otherwise, EUR will be used.

Would you like to become a TWINO investor? Then press the button below and sign up. It’s the easiest way to go from reading this TWINO review, to actually investing yourself:

How to invest on TWINO?

Before you can start investing on TWINO, you must complete the following steps:

- Sign up on the TWINO website.

- Verify your identity.

- Complete the KYC questionnaire.

- Deposit funds into your account.

The entire registration process usually takes about 5-10 minutes, including signing up, verifying your identity, filling out any required questionnaires, and making your first deposit.

You can deposit money into your TWINO account using SEPA transfers. The minimum deposit is €0.01, and funds typically arrive within 1-3 business days. It is only possible to deposit funds in Euros (EUR).

Once you have funded your account, you can start investing in P2P loans on the platform. TWINO allows you to invest manually by browsing available loans or automatically using an auto-invest strategy.

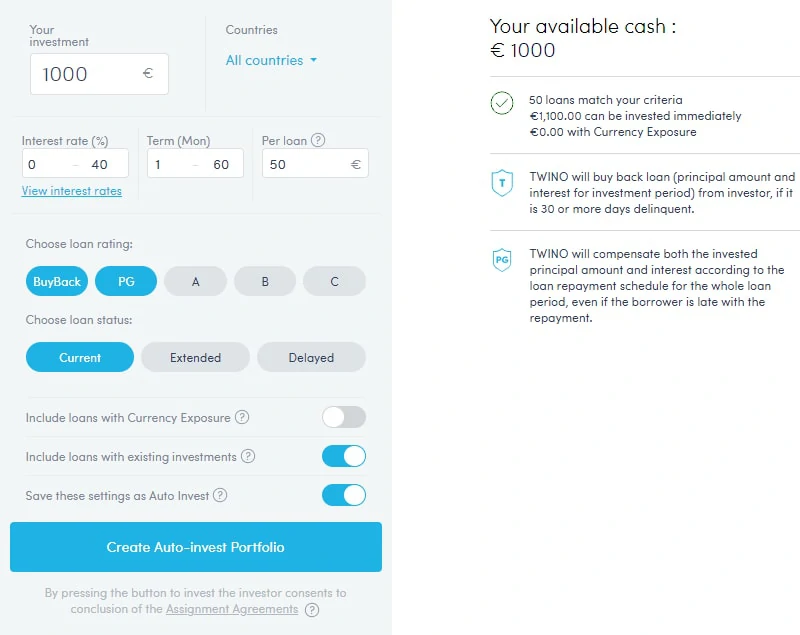

TWINO auto-invest

TWINO provides an auto-invest feature to automatically allocate funds into suitable loan investments based on each investor’s predefined criteria, saving time and simplifying the investment process.

The auto-invest tool enables you to configure key parameters, including portfolio size, maximum investment per loan, interest rate, loan term, loan type, loan status, countries, and loan originators. You can also automatically reinvest all returns.

Setting up a TWINO auto-invest strategy only takes 1 minute, and your funds should be invested within a few hours. If your auto-invest is not working, it is usually due to a lack of loans that meet your criteria. This can happen when your filters are too narrow or when no suitable loans are available.

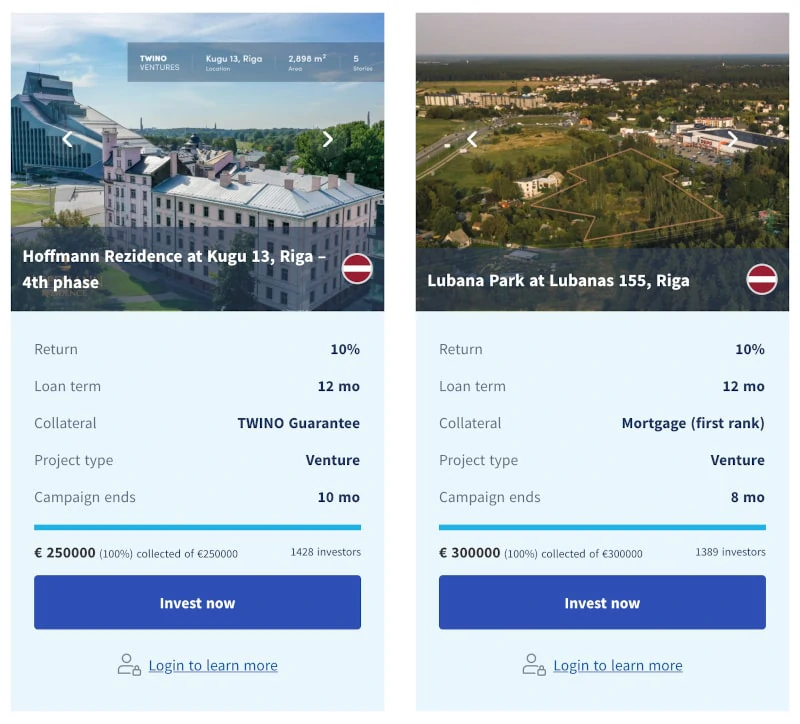

TWINO Ventures

In 2020, TWINO introduced a real estate focused addition to its platform that is similar to that of some of the best real estate crowdfunding platforms in Europe.

This was called TWINO Ventures and allows investors on the platform to invest in property-focused projects like the following:

As you can see in the image above, this feature has become very popular with over 1,000 investors per project. You can learn more about TWINO Ventures on the website:

How to withdraw money from TWINO?

You can withdraw your uninvested funds from TWINO at any time using the withdrawal section of your investor account. The minimum withdrawal amount is €0.01 and it usually takes 1-2 business days for your funds to arrive in your bank account.

TWINO does not charge any fees for withdrawing funds from your account, but your bank may charge fees for receiving international transfers.

To exit TWINO, you must first turn off all auto-invest strategies and sell any existing loans on the secondary market. If you hold non-performing loans, the platform must first recover the underlying debt before allowing withdrawals, which can negatively affect your liquidity.

TWINO secondary market

TWINO offers a secondary market for all its investments, enabling investors to sell their loans before maturity. The TWINO secondary market does not have any fees for either buyers or sellers.

The time it takes to sell investments on the TWINO secondary market varies based on the price set by the seller and current market conditions. Sellers have the flexibility to list loans at face value or apply discounts or premiums to draw in buyers. The discount rate is capped at 29.9%, while the premium cannot exceed 4.9%. Loans that are defaulted cannot be listed on the secondary market.

While TWINO offers a free and fairly liquid secondary market, Mintos can be a better alternative for investors seeking to maximize liquidity and uncapped premiums, although it does charge a 0.85% selling fee.

What are the best TWINO alternatives?

Some of the best alternatives to TWINO are Mintos, Esketit and Swaper.

Conclusion of our TWINO review

TWINO is a moderately appealing P2P lending platform due to its transparent financial reporting and a profitable track record that offers comfort to investors. The platform sets itself apart from competitors by openly sharing detailed financial statements and expanding into real estate funding through TWINO Ventures, which provides additional investment opportunities beyond short-term consumer loans.

While TWINO presents competitive returns, a user-friendly interface, and buyback or payment guarantees on most loans, it has also faced loan availability issues, a higher percentage of defaults, and lingering concerns about buyback reliability.

TWINO might be worth it for investors who seek moderate-to-high returns in a platform with a profitable track record and can handle occasional loan shortages or repayment delays. It might not be a good investment for those who prioritize consistent loan selection or a more robust regulatory framework. If you prefer a platform with deeper loan variety or are risk-averse, consider alternative P2P lending platforms.

Do you want to sign up for their platform after reading our TWINO review? Then simply click on the button below. This will take you directly to TWINO’s website, where you can sign up and start investing in their listed loans: