Mintos review 2025

In this comprehensive Mintos review, you’ll find an overview of the platform’s key advantages and disadvantages, along with an in-depth analysis of its core features, potential returns, safety measures, and overall user experience to help you determine whether Mintos aligns with your investment strategy.

Mintos

Pros

Cons

Mintos review summary:

Mintos is one of the leading peer-to-peer (P2P) lending marketplaces in Europe, headquartered in Riga, Latvia. Since its inception in 2015, Mintos has grown to become a significant platform connecting investors with borrowers from around the world through various loan originators. The platform provides an opportunity for investors to diversify their portfolios by investing in loans of different types and from multiple countries.

It’s 100% free to open an account

Introduction to our Mintos review

Is Mintos safe? We’ve invested in this European P2P lending platform for a while to find out. In this Mintos review, you’ll learn our thoughts on the platform’s performance, tips for maximizing returns, and how we rate its safety. Feel free to skip ahead if you’re short on time. Please note that this review is based solely on our experience and does not constitute financial advice.

Learn about the following in our Mintos review:

- What is Mintos?

- Is it safe to invest on Mintos?

- What is the return on Mintos?

- What are the fees on Mintos?

- Who can invest on Mintos?

- How to invest on Mintos?

- How to withdraw money from Mintos?

- What are the best Mintos alternatives?

- Conclusion of our Mintos review

What is Mintos?

Mintos is a peer-to-peer (P2P) lending platform headquartered in Riga, Latvia. Launched in 2015 by co-founders Martins Sulte and Martins Valters, it has grown to become Europe’s largest P2P lending platform, attracting more than 500,000 investors who have collectively funded over €10.9 billion in loans.

Mintos works by connecting individual investors with a range of loan originators across multiple countries. Investors can choose loans based on their preferences for risk and return, then provide funding starting from as little as €50.

AS Mintos Marketplace is regulated and operates under licenses granted by the Financial and Capital Market Commission (FCMC) in Latvia.

Key points about Mintos:

- Mintos is the largest P2P lending platform in Europe.

- Mintos is one of the best platforms for broad diversification.

With a minimum investment of €50, you can easily try out the platform at www.mintos.com.

Mintos statistics:

| Launched: | 2015 |

| Investors: | 522,300 + |

| Interest rate: | 5 – 30 % |

| Loan period: | 1 – 80 months |

| Loan type: | Consumer |

| Loans funded: | € 9,100,000,000 + |

| Min. investment: | € 50 |

| Max. investment: | Unlimited |

Mintos Trustpilot rating

Mintos has received a TrustScore of 4.1/5 based on 4,123 reviews on Trustpilot. Investors commend its diverse offering (loans, bonds, ETFs), user-friendly interface, and frequent updates, as well as generally responsive support. However, some reviewers cite concerns about defaults, slower-than-expected recovery processes, and occasional technical glitches.

Is it safe to invest on Mintos?

Mintos is considered one of the safest P2P lending platforms in Europe. It has been operating reliably since 2015, with a low default rate of 0.1% for investors. 80.9% of the loans on Mintos are current and most loans on the platform include a buyback guarantee, providing an added layer of protection against borrower default.

Licensed and regulated

AS Mintos Marketplace is regulated and operates under licenses from the Financial and Capital Market Commission (FCMC) in Latvia. Its regulated status indicates that Mintos is legitimate and not a scam.

Insolvency protection

Mintos participates in the national investor compensation scheme of the Republic of Latvia, aligned with the EU Directive 97/9/EC. If the platform becomes insolvent and cannot provide investment services, retail investors are eligible for compensation covering 90% of any irreversible loss, up to a maximum of €20,000.

Mintos is required to keep investor funds separate from its own account, which means that in the event of insolvency, investor funds are safeguarded and cannot be accessed by creditors to settle Mintos’ debts.

Mintos loan originators

Mintos has 64 loan originators in 34 countries that deal in 10 different loan types, making it the top marketplace for diversification.

Mintos requires loan originators to retain 2-30% skin in the game on each loan, with most aligning to the industry norm of 5-10%. By holding a portion of the loan themselves, originators share the risk with investors. This shared responsibility typically encourages more careful underwriting and discourages reckless lending practices.

More than 22 loan originators on Mintos have been suspended since the platform’s inception, suggesting a higher-than-anticipated risk for investors. This figure underscores the need for thorough due diligence before committing capital. It also highlights the importance of monitoring loan originator performance and updates from the platform.

Collateral

Mintos provides investments in both unsecured and secured loans. With secured loans, the collateral may vary based on the loan type. For example, mortgage loans can be backed by real estate, car loans by vehicles, or business loans by equipment. Other forms of collateral may also apply, as specified under each individual loan on the platform.

Mintos buyback obligation

On Mintos, most loans are covered by a 60-day buyback obligation. This means that if a borrower is more than 60 days late with repayments, the loan originator automatically repurchases the loan from the investor along with accrued interest.

The Mintos buyback guarantee has a duration of 60 days, which is the industry standard. This is longer compared to Robocash and Loanch, which offer the shortest buyback duration on the market at 30 days.

Investors should keep in mind that the reliability of the Mintos buyback obligation depends on the financial stability of the loan originators. If the loan originators are unable to buy back the loans, the buyback guarantee becomes worthless.

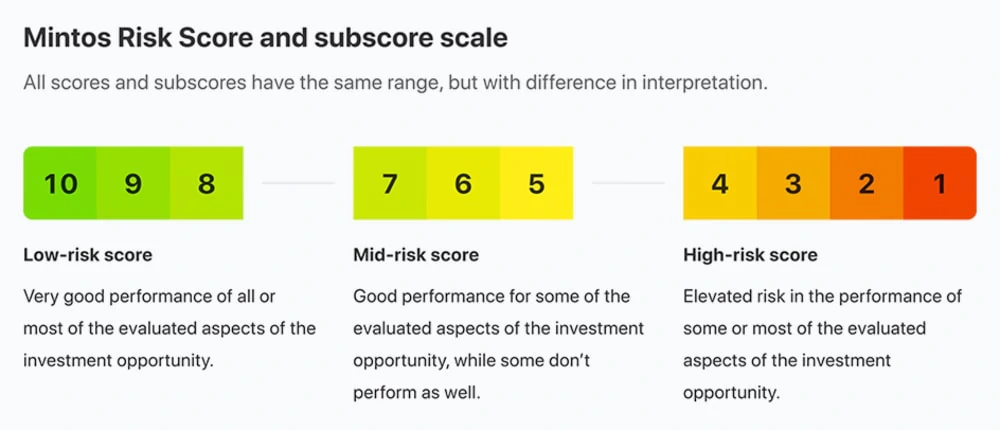

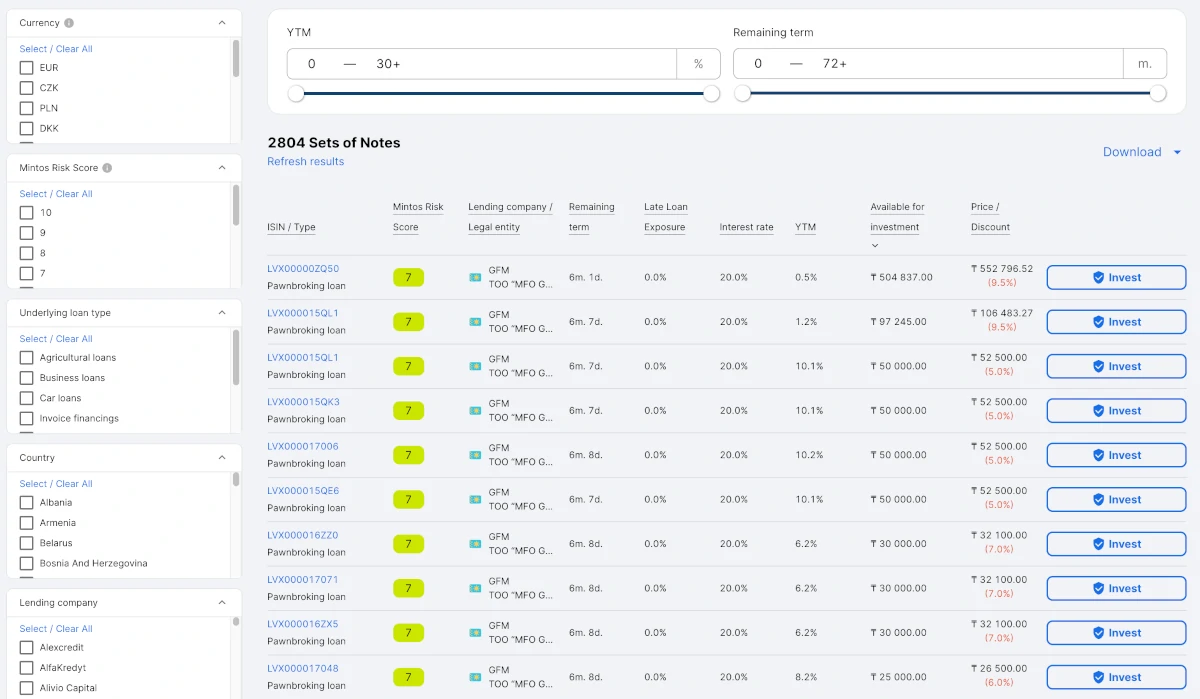

Mintos Risk Score

In 2018, Mintos became the first P2P lending platform in Europe to introduce loan originator credit ratings. A few years later, in 2020, they decided to upgrade the rating systems and Mintos Ratings became Mintos Risk Score.

The risk score ranges from 1 to 10. The loan originators with some of the highest scores (8-10) are the ones with the lowest risk. The highest risk is for those loan originators with the lowest scores (1-4). Below you can see a visualization of the score scale:

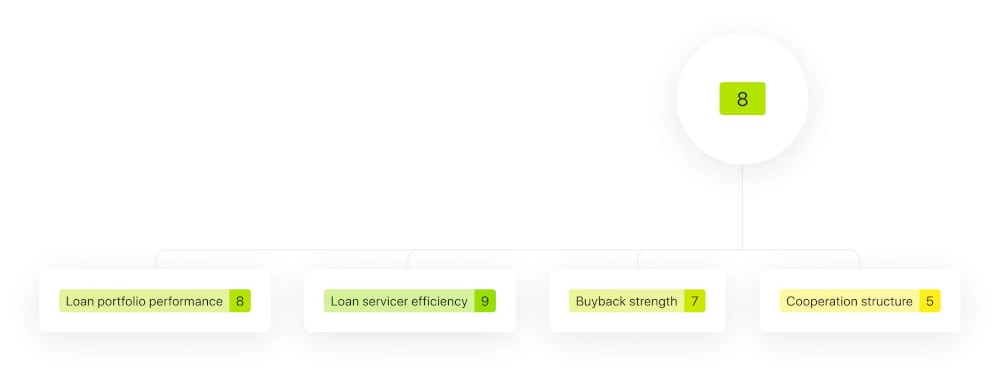

The Mintos Risk Score is based on 4 subscores that are weighted as follows:

- 40% loan portfolio performance

- 25% loan servicer efficiency

- 25% buyback strength

- 10% cooperation structure

In a case where a company has received the Risk Score of 8, the subscores could look like the following:

Updates to the scores are made 4 times a year on a quarterly basis.

According to the Mintos Risk Score, roughly speaking, loans with low risk (8-10) should be safer than loans with moderate risk (5-7), which should be safer than loans with high risk (1-4).

Two-factor authentication

Mintos offers two-factor authentication (2FA) to strengthen account security. This feature works with the Google Authenticator app, generating unique, time-based passcodes that protect investor funds from unauthorized access. Since hackers have targeted P2P lending platforms in the past, enabling 2FA is strongly recommended.

What is the return on Mintos?

Mintos’s average annual investment return is around 12.25%. This puts the platform in the mid-range when compared to other P2P lending platforms, where common rates often lie between 9% and 15%. Actual outcomes can vary based on loan performance and individual strategies.

The interest rates on Mintos ranges from 5% to 22%, which indicates a broad spectrum of risk. Higher-interest loans often carry a greater chance of default, so while returns may be enticing, investors should be prepared for the possibility of stalled repayments or the need for buyback guarantees.

Time-limited welcome bonus

Readers of this Mintos review are eligible for a €25 cashback bonus. To unlock this offer, new investors must sign up using the button below and invest at least €1,500 within 30 days. No Mintos promo code is required.

What are the fees on Mintos?

Mintos does not charge fees for investing, depositing, or withdrawing funds. However, fees apply for Mintos loan portfolios, Mintos Smart Cash, currency exchanges, secondary market sales, and inactivity after six months.

- Mintos portfolios: 0.39% p.a.

- Mintos Smart Cash: 0.19% p.a.

- Currency exchange: From 0.50% depending on currency pair

- Secondary market: 0.85% for selling investments

- Inactivity fee: €2.90 per month after 6 months

Mintos has a more complex fee structure compared to main competitors like PeerBerry, VIAINVEST, TWINO, Robocash and Esketit, which have zero fees for investors. This makes it harder for investors to estimate returns after fees.

Does Mintos withhold taxes?

Mintos is legally required to withhold taxes on interest income from loans on its platform. This can make handling your taxes more complex than on platforms such as PeerBerry, Robocash, or Esketit, which do not withhold taxes.

The standard withholding tax rate on Mintos is 5% for EU/EEA tax residents and 25.5% for all others, including Latvian tax residents. Investors from Lithuania can reduce their tax rate to 0% by providing a valid tax residency certificate.

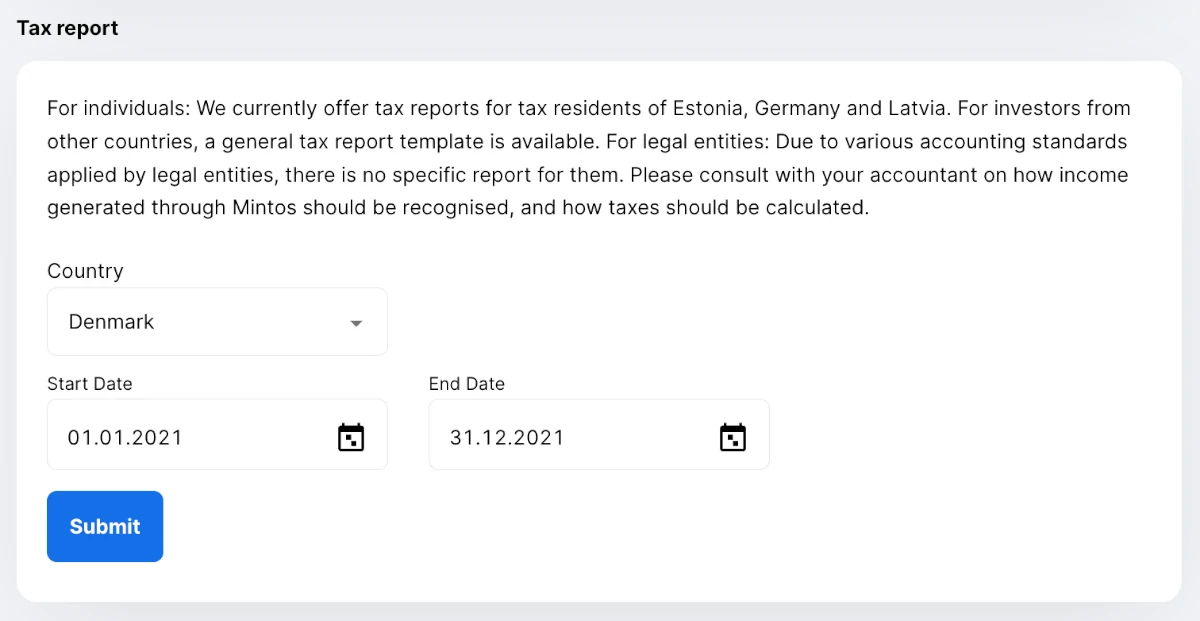

Tax report

Mintos provides a tax report to help you declare your earnings to local authorities. You can easily download your income statement from your dashboard on the Mintos platform.

Who can invest on Mintos?

It is both possible for individuals and companies to invest with Mintos. This makes the platform an obvious choice whatever the structure of your economy is.

Individuals

As an individual, there are a few, but clear rules for what it takes to enable you to invest through the platform:

- Minimum age of 18 years

- Bank with AML / CFT equivalent to the EU

- Agree with the Mintos user agreement

- Successfully verified your identity by Mintos

If you live up to the above requirements as an individual, you can invest through the platform.

Companies

If you would like to invest as a company, this is also possible. To open a Mintos business account, it is also required that you have a bank account in the European Union and that your company is registered in the EU or third countries that have AML / CFT systems similar to those found in the EU.

Would you like to sign up as a Mintos investor? Then click the button below to go from reading this Mintos review to actually investing on their platform:

How to invest on Mintos?

Before you can start investing on Mintos, you must complete the following steps:

- Sign up on the Mintos website.

- Verify your identity.

- Complete the KYC questionnaire.

- Deposit funds into your account.

The entire registration process usually takes about 5-10 minutes, including signing up, verifying your identity, filling out any required questionnaires, and making your first deposit.

You can deposit money into your Mintos account using SEPA and SWIFT transfers, as well as third-party payment services like Wise or Revolut. The minimum deposit is €0.01, and funds typically arrive within 1-5 business days. It is possible to deposit funds in multiple currencies, but keep in mind that Mintos charges a currency exchange fee starting at 0.5%, depending on the currency pair.

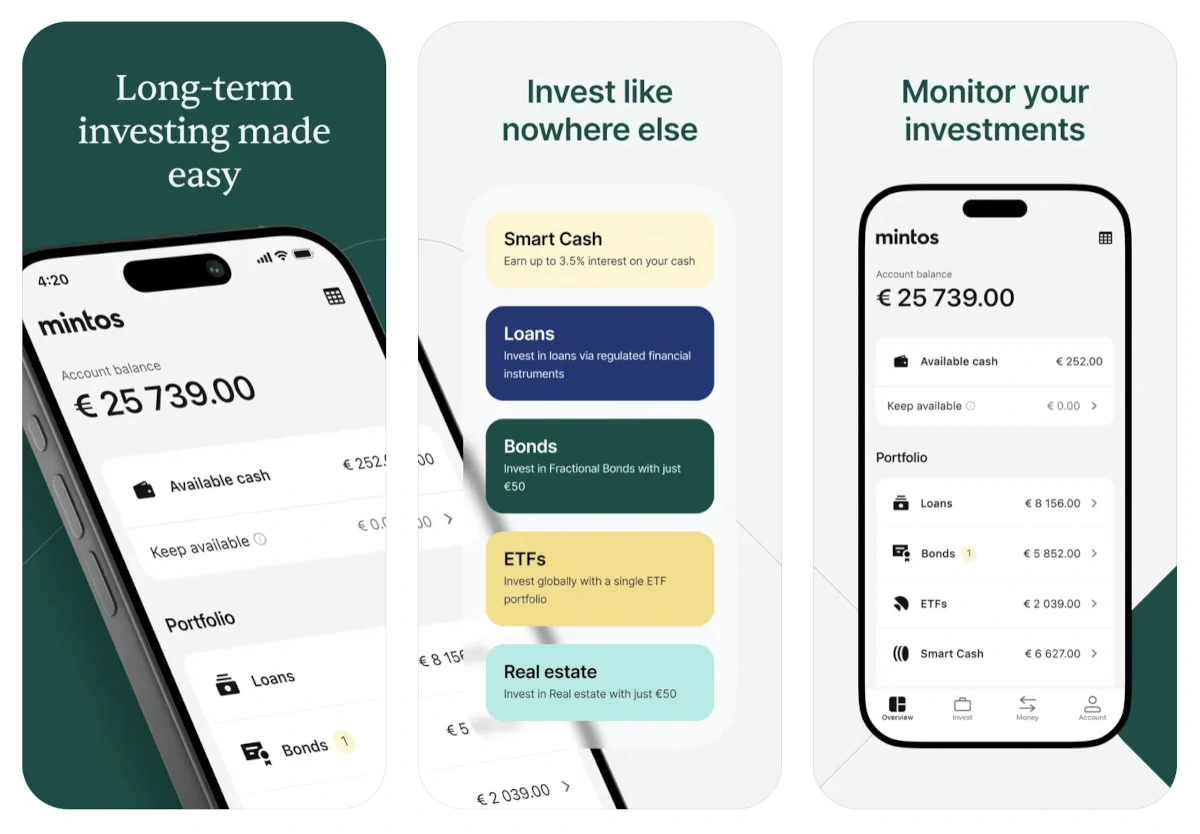

Once you have funded your account, you can start investing in a wide range of assets on the platform, including loans, bonds, ETFs, real estate, and money market funds.

Mintos allows you to invest manually by browsing available loans or automatically using a predefined or custom auto-invest strategy.

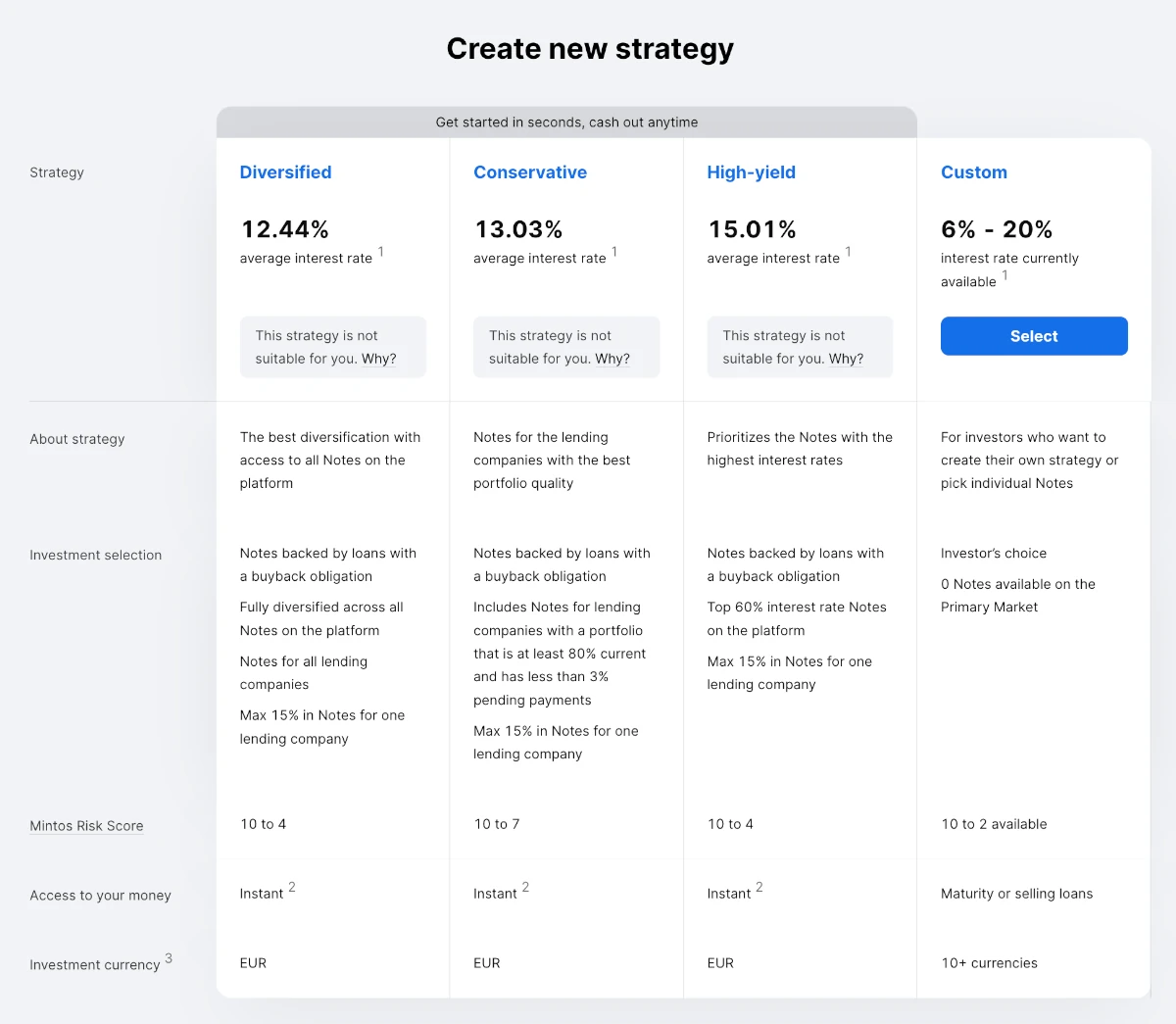

Mintos strategies

Mintos strategies are 3 new automated investment strategies launched in August 2020. These strategies are the next generation of what was formerly known as Mintos Invest & Access.

The three Mintos investment strategies are:

- Diversified (the old Mintos Invest & Access strategy)

- Conservative

- High-yield

In the following, you can see how the 3 Mintos investment strategies (on the left-hand side) compare to making a custom strategy on Mintos:

A huge advantage of using one of the three strategies instead of making a custom strategy is the fact that you won’t have to continuously add new loan originators to your auto-invest settings as they are connected to the marketplace.

This makes the Mintos investment strategies an excellent choice if you want the most hands-off investment experience.

The biggest drawback of using Mintos strategies, instead of a custom auto-investment strategy, is that you won’t be able to tailor the investment strategy as much. However, this has improved tremendously since Mintos Invest & Access, as you now have three different strategies to choose from instead of one.

With that said, going with a Mintos strategy is probably the best choice for new investors that are not certain that they want to have their money tied up on the platform yet. This is due to the very fast access to your money if you want to sell your investments.

Mintos auto-invest

Mintos provides an auto-invest feature to automatically allocate funds into suitable loan investments based on each investor’s predefined criteria, saving time and simplifying the investment process.

The auto-invest tool enables you to configure key parameters, including portfolio size, maximum investment per loan, interest rate, loan term, loan type, loan status, countries, and loan originators. You can also automatically reinvest all returns.

Setting up a Mintos auto-invest strategy only takes 1 minute, and your funds should be invested within a few hours. If your auto-invest is not working, it is usually due to a lack of loans that meet your criteria. This can happen when your filters are too narrow or when no suitable loans are available.

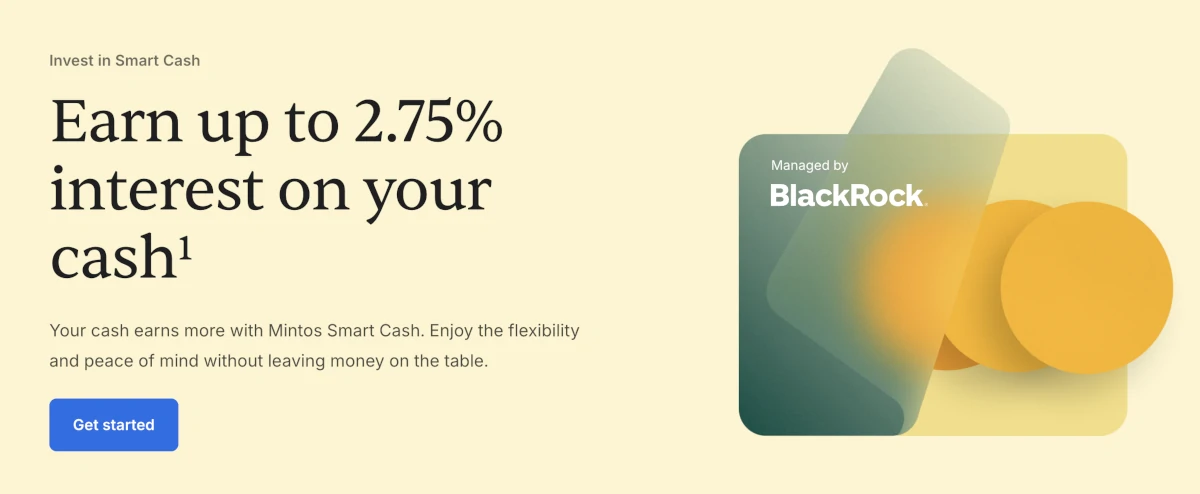

Mintos Smart Cash

Mintos Smart Cash is an option for those seeking a higher return on idle cash with flexibility and easy withdrawals, although it does carry some investment risk and is not covered by deposit insurance. It offers a target interest of up to 2.25% and provides same-day access to your funds without fees or penalties. While it isn’t guaranteed like a bank deposit, it carries relatively low risk due to diversification in high-quality, short-term securities. Fees include a 0.10% annual BlackRock management fee plus Mintos’s fee of 0.19% per annum from the interest.

Mintos app

Mintos provides a dedicated mobile app for both Android and iOS devices. This feature sets Mintos apart, as only a handful of its competitors currently provide mobile apps.

The Mintos app allows you to review your portfolio and track your returns in near real-time. You can also set up and manage your auto-invest strategies on the go.

The app has a medium rating of 3.7 out of 5 stars and has been downloaded over 100,000 times, making it a decent option for on-the-go investors.

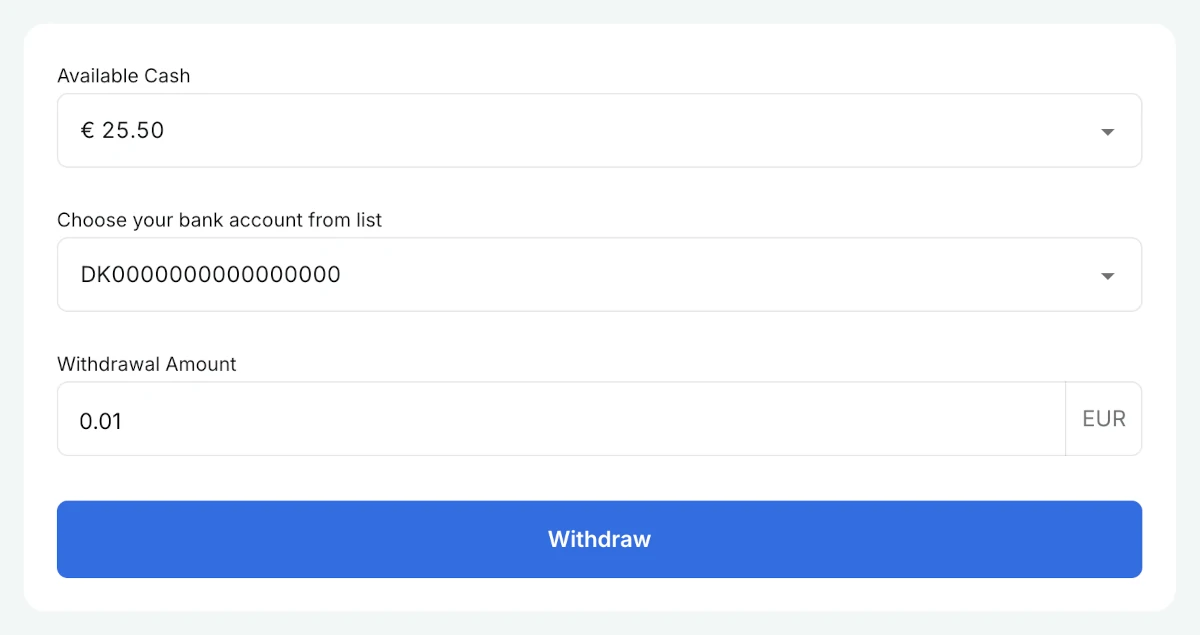

How to withdraw money from Mintos?

You can withdraw your uninvested funds from Mintos at any time using the withdrawal section of your investor account. It usually takes 1-2 business days for your funds to arrive, unless your bank supports SEPA Instant, which reduces the withdrawal time to 30 minutes. The minimum withdrawal amount is €0.01.

Mintos does not charge any fees for withdrawing funds from your account, but your bank may charge fees for receiving international transfers.

To exit Mintos, you must first turn off all auto-invest strategies and sell any existing loans on the secondary market. If you hold non-performing loans, the platform must first recover the underlying debt before allowing withdrawals, which can negatively affect your liquidity.

Mintos secondary market

Mintos offers a secondary market for investments in Notes, giving investors the opportunity to sell their holdings. While sellers pay a 0.85% transaction fee, buyers can use the secondary market at no cost.

The secondary market on Mintos stands out as the most active in Europe with over 65 million transactions made by over 420,000 investors. The time it takes to sell investments depends on the price set by the seller and current market conditions. Sellers have the flexibility to list loans at face value or to apply discounts or premiums to attract potential buyers.

While Mintos offers the most liquid secondary market, you can find great alternatives without a selling fee, including Robocash, Swaper, Esketit and TWINO.

What are the best Mintos alternatives?

Some of the best alternatives to Mintos are Robocash, PeerBerry and Esketit.

Conclusion of our Mintos review

Mintos is one of the best P2P lending platforms in Europe for broad diversification. The platform sets itself apart from competitors through its comprehensive risk assessment of loan originators and transparent reporting of financial performance.

While Mintos provides a regulated environment, a wide range of loan originators, and an industry-standard buyback obligation, the lengthy recovery process for defaulted loan originators and a more complex fee structure can impact returns and liquidity.

Mintos might be worth it for investors seeking broad diversification and comfortable navigating the risks required to achieve higher returns. It might not be a good investment for risk-averse individuals who prefer a simpler fee structure and a lower chance of defaults causing long recovery periods.

Do you want to invest through the platform after reading our Mintos review? Then click on the button below to get to their website and create an account: