FinBee review 2025

Check out our FinBee review, and see if the platform is for you.

FinBee

Pros

Cons

FinBee review summary:

FinBee is excellent for P2P lending. They have above-average skin in the game and offer above-average interest rates. It is also easy to try them out with a low minimum deposit of only €5. However, most of the loans on the platform are not secured, which is why we don’t recommend FinBee for beginners. Consider a platform like Lendermarket or Swaper instead.

It’s 100% free to open an account

Introduction to our FinBee review

FinBee offers impressive returns, but is it truly worth using? Our FinBee review delves into its pros and cons to help you decide. If you’re considering investing, we suggest reading it first — you’ll get a clearer picture of the platform. Remember, though, everything here reflects our own opinion and is not financial advice.

Learn about the following in our FinBee review:

- What is FinBee?

- What is the return on FinBee?

- Is it safe to invest on FinBee?

- Who can invest on FinBee?

- How to invest on FinBee?

- How to withdraw money from FinBee?

- What are the best Finbee alternatives?

- Conclusion of our FinBee review

What is FinBee?

FinBee is a Lithuanian peer-to-peer lending platform that launched in August 2015. It connects investors with consumer and business loan borrowers in Lithuania, offering advertised returns of up to 18%.

FinBee works by allowing individuals and legal entities to invest in parts of various loans. You set how much you want to invest, and FinBee pools your funds with other investors’ contributions to finance loans. This setup aims to spread risk and provide a consistent return on your investment.

The platform has a community of more than 30,000 investors and has funded over €114 million in loans since its inception.

FinBee is regulated. It holds a crowdfunding investment license under the supervision of the National Bank of Lithuania, ensuring that it meets local financial and compliance standards.

FinBee statistics:

| Launched: | 2015 |

| Investors: | 30,000 + |

| Interest rate: | 10 – 26 % |

| Loan period: | 12 – 60 months |

| Loan type: | Consumer |

| Loans funded: | € 114,000,000 + |

| Min. investment: | € 10 |

| Max. investment: | Unlimited |

Finbee Trustpilot rating

Finbee has received a TrustScore of 3.5/5 based on 0 reviews on Trustpilot.

What is the return on FinBee?

FinBee’s average annual investment return is 15.3%. This places the platform near the top end among P2P lending options, where many peers offer returns closer to 9–12%. Higher returns generally suggest a higher risk profile, so potential investors should weigh the possibility of borrower defaults against these attractive rates.

The interest rates on FinBee ranges from 10% to 22%, giving investors the opportunity to choose between moderate and higher-risk loans. While the upper end of that range can lead to more substantial returns, it also reflects an increased risk that not all investors may find suitable.

Is it safe to invest on FinBee?

FinBee is not considered one of the safest P2P lending platforms in Europe, mainly due to its lack of transparency about loan performance and the absence of any buyback guarantee to protect investors from potential losses. Without this extra safety net, investors confront a higher risk of non-repayment, which makes FinBee a less reliable option compared to other platforms offering more robust safeguards.

FinBee is regulated and holds a crowdfunding investment license under the supervision of the National Bank of Lithuania. This regulatory oversight indicates that FinBee meets proper local financial and compliance standards, suggesting that the platform is legit and not a scam.

Skin in the game

FinBee is keeping a stake of at least 12% in all consumer loans on the platform. The fact that they have skin in the game with the investors is a positive signal, as it is then in their best interest to provide maximum safety and return for themselves and the investors. It shows that they have confidence in their own loans.

The 12% skin in the game is quite high compared to other platforms, where it is usually around 5-10%. However, if you’d like a higher amount of skin in the game, you should check out our Iuvo Group review. On that platform, loan originators have 30% skin in the game, but the return is also lower.

Collateral

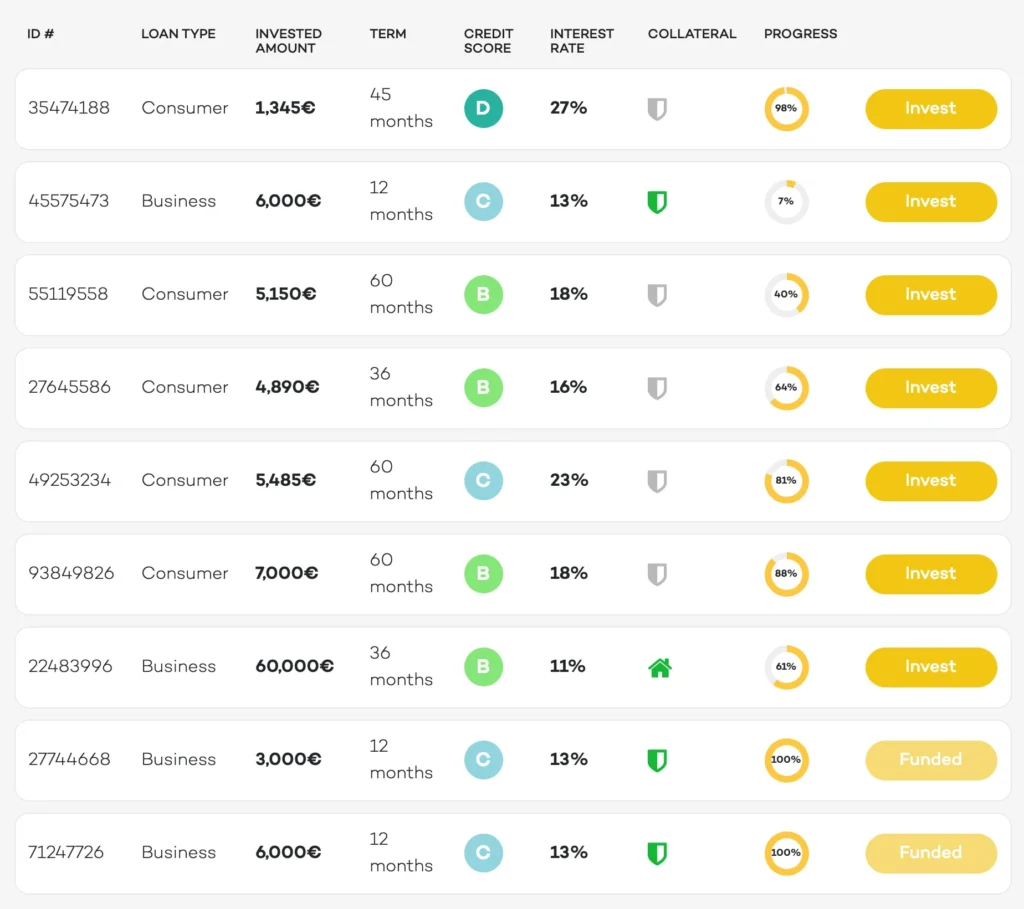

On FinBee’s platform, most loans are not covered by any collateral or guarantees. However, you will be able to find it on some of the loans. In the following, you can see a selection of the loans on the marketplace:

In the collateral column, you will be able to see if a loan is covered by any form of collateral. Most loans aren’t covered by any guarantees.

- Grey shield = no guarantee

- Green shield = some guarantee

- Green house = real estate collateral

Due to the fact that there is no collateral on most loans on FinBee, it might be a good idea for beginner investors to consider other P2P lending platforms that offer more guarantees. But if you are comfortable with the fact that some of your investments will default, FinBee might still be a viable option for you.

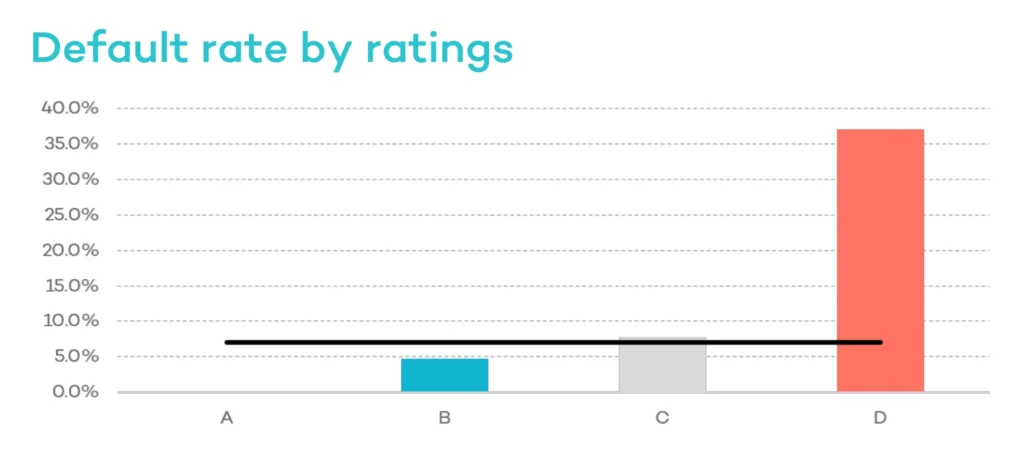

Borrower ratings

In order to give you an idea of the safety of a particular loan on the platform, FinBee provides borrower ratings for all loans. It is crucial that you understand these before you invest.

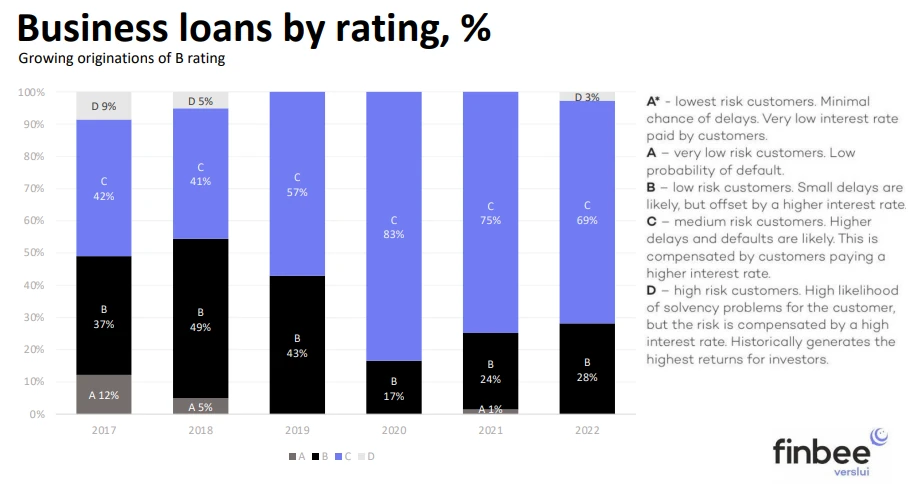

The ratings go from A to D, where A involves the least risk, and D involves the most risk. In the following, you can see the default rates by category for business loans:

As you can see, there is a substantial difference between loans with an A-rating (with around 0% defaults) and a loan with a D-rating (with over 35% defaults) when it comes to risk. So even though it on the surface can seem like a good idea to invest in loans with a D-rating when you look at the loan list on the website, it will involve a lot of defaults.

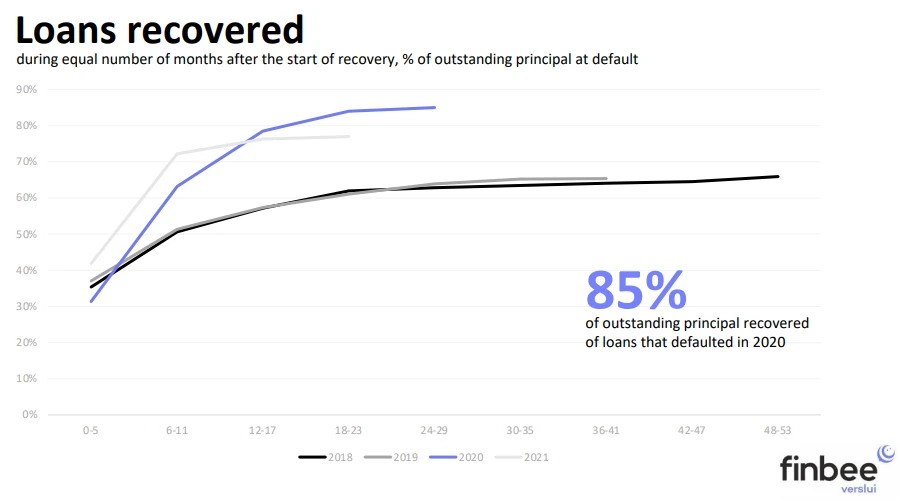

But even though a lot of investments with a D-rating will face default, the team at FinBee actually manages to recover quite a bit of these, as shown in the recovery rates below:

As of Q3 2022, there is a growing number of business loans with B and C ratings:

But even though there are a lot of loans that are recovered after the default, you simply need to consider the default rates by rating before you invest on the platform.

Please keep in mind that all the above examples only are for business loans. You can learn more about the numbers for consumer loans here.

Who can invest on FinBee?

In order to invest via FinBee you must meet the following requirements:

- Be a least 18 years old

- Have a European bank account in your name

- Have a valid ID

If you meet the above requirements, it is easy to get started at FinBee. Simply follow the steps below, and then you should rather quickly be able to invest:

- Create an account

- Answer the KYC (Know-Your-Customer) questionnaire

- Validate your identity

- Add funds to your account

- Invest in loans from the loan list

Do you meet the requirements to sign up as an investor at FinBee? Then press the button below to get to their website. From here you can quickly create yourself a free account and get started investing:

How to invest on FinBee?

Before you can start investing on FinBee, you must complete the following steps:

- Sign up on the FinBee website.

- Verify your identity.

- Complete the KYC questionnaire.

- Deposit funds into your account.

The entire registration process usually takes about 5-10 minutes, including signing up, verifying your identity, filling out any required questionnaires, and making your first deposit.

You can deposit money into your FinBee account using SEPA and SWIFT transfers. The minimum deposit is €0.01, and funds typically arrive within 1-3 business days.

Once you have funded your account, you can start investing in P2P loans on the platform. FinBee allows you to invest manually by browsing available loans or automatically using an auto-invest strategy.

FinBee auto-invest

FinBee provides an auto-invest feature to automatically allocate funds into suitable loan investments based on each investor’s predefined criteria, saving time and simplifying the investment process.

The auto-invest tool enables you to configure key parameters, including portfolio size, maximum investment per loan, interest rate, loan term, loan type, loan status, countries, and loan originators. You can also automatically reinvest all returns.

Setting up a FinBee auto-invest strategy only takes 1 minute, and your funds should be invested within a few hours. If your auto-invest is not working, it is usually due to a lack of loans that meet your criteria. This can happen when your filters are too narrow or when no suitable loans are available.

How to withdraw money from FinBee?

You can withdraw your uninvested funds from FinBee at any time using the withdrawal section of your investor account. The minimum withdrawal amount is €0.01 and it usually takes 1-2 business days for your funds to arrive in your bank account.

FinBee does not charge any fees for withdrawing funds from your account, but your bank may charge fees for receiving international transfers.

To exit FinBee, you must first turn off all auto-invest strategies and sell any existing loans on the secondary market. If you hold non-performing loans, the platform must first recover the underlying debt before allowing withdrawals, which can negatively affect your liquidity.

FinBee secondary market

FinBee offers a secondary market for all its investments, enabling investors to sell their loans before maturity. There are no additional fees for buyers or sellers in the secondary market, apart from the monthly €1 account fee.

The time it takes to sell investments on the FinBee secondary market varies based on the price set by the seller and current market conditions. Sellers can list loans at their face value or attach a discount or premium to attract potential buyers. Each listing remains valid until the loan’s next scheduled payment, after which the seller must create a new listing.

Loans that are late cannot be listed on the secondary market.

What are the best FinBee alternatives?

Some of the best alternatives to FinBee are Hive5, PeerBerry and NEO Finance.

Conclusion of our FinBee review

FinBee is a good P2P lending platform for experienced investors seeking above-average returns and a meaningful stake from the platform itself. It sets itself apart by offering at least 12% skin in the game on consumer loans, aligning FinBee’s interests with its investors.

While FinBee provides attractive average returns of 15.3%, a low minimum deposit, and a regulated environment under the National Bank of Lithuania, it lacks a buyback guarantee and involves higher risk due to many unsecured loans.

FinBee is worth considering for investors who understand the importance of creating a careful risk strategy and are comfortable with the possibility of defaults. It might not be a good fit for beginners or risk-averse individuals who prefer loans with strong collateral or regular buyback guarantees. If you prioritize more robust protections and lower default rates, consider other P2P lending platforms.