Bondster review 2025

Read this Bondster review to learn if you should use the platform.

Bondster

Pros

Cons

Bondster review summary:

Bondster offers competitive returns, flexible diversification, and user-friendly investing features backed by a strong parent company. However, it is unregulated, has reports of questionable loan originators, and varying buyback reliability. It suits higher-yield seekers who can accept moderate to high risk, but risk-averse investors may prefer a regulated platform with more consistent buyback protections.

It’s 100% free to open an account

Introduction to our Bondster review

Considering Bondster? Check out our Bondster review for an honest look at its pros and cons. You can skip ahead using the navigation or read the whole thing. This article reflects our opinion only and does not constitute financial advice.

Learn about the following in our Bondster review:

- What is Bondster?

- Is it safe to invest on Bondster?

- What is the return on Bondster?

- What are the fees on Bondster?

- Who can invest on Bondster?

- How to invest on Bondster?

- How to withdraw money from Bondster?

- What are the best Bondster alternatives?

- Conclusion of our Bondster review

What is Bondster?

Bondster is a Czech-based peer-to-peer lending marketplace that launched in May 2017. It allows investors to fund secured and unsecured loans from various external lending companies, with advertised returns of up to 17%.

Bondster works by allowing investors to open an account on the Bondster platform and choose from different loan offers based on loan type, duration, and interest rate. Once an investor commits funds to a loan, they earn interest as the borrower makes repayments, while Bondster facilitates the transaction and provides loan monitoring services.

Over 21,000 investors are registered on Bondster, and they have collectively provided more than €217 million in loan funding.

BONDSTER Marketplace s.r.o. is not regulated, as it is not required in the jurisdiction in which it operates.

Bondster statistics:

| Launched: | 2017 |

| Investors: | 21,000 + |

| Interest rate: | 8 – 17 % |

| Loan period: | 1 – 12 months |

| Loan type: | Consumer |

| Loans funded: | € 217,000,000 + |

| Min. investment: | € 5 |

| Max. investment: | Unlimited |

Bondster Trustpilot rating

Bondster has received a TrustScore of 2.5/5 based on 106 reviews on Trustpilot. While some users praise its varied loan offerings, potential for high returns, and occasional successful recoveries, others report frustration with unfulfilled buyback guarantees, prolonged recovery times, and limited communication concerning delayed or defaulted loans. Despite these concerns, several investors still highlight the advantages of diversifying on Bondster to mitigate risks and maintain a steady return.

Is it safe to invest on Bondster?

Bondster is not considered one of the safest P2P lending platforms in Europe, primarily due to a history of questionable loan originators and limited transparency about loan performance. While 85% of its loans come with a buyback guarantee, some investors on Trustpilot question the reliability of this feature, indicating that its effectiveness might be inconsistent.

Since BONDSTER Marketplace s.r.o. is not regulated, it may be perceived as riskier compared to regulated platforms. While the company behind the platform appears to be legitimate and not a scam, potential investors should carefully assess the associated risks and do further due diligence before committing any funds.

Loan originators

Bondster has 34 loan originators in 20 countries that deal in 10 different loan types, making it one of the best marketplaces for broad diversification.

Bondster requires loan originators to retain 2-20% skin in the game on each loan, with most aligning to the industry norm of 5-10%. By holding a portion of the loan themselves, originators share the risk with investors. This shared responsibility typically encourages more careful underwriting and discourages reckless lending practices.

Bondster buyback guarantee

On Bondster, 85% of loans are covered by a 30- or 60-day buyback guarantee. This means that if a borrower is more than 30 or 60 days late with repayments, the loan originator automatically repurchases the loan from the investor along with accrued interest.

The Bondster buyback guarantee has a duration of 30-60 days, which is close to the industry standard of 60 days. This can be longer compared to Robocash and Loanch, which offer the shortest buyback duration on the market at 30 days.

Investors should keep in mind that the reliability of the Bondster buyback obligation depends on the financial stability of the loan originators. If the loan originators are unable to buy back the loans, the buyback guarantee becomes worthless.

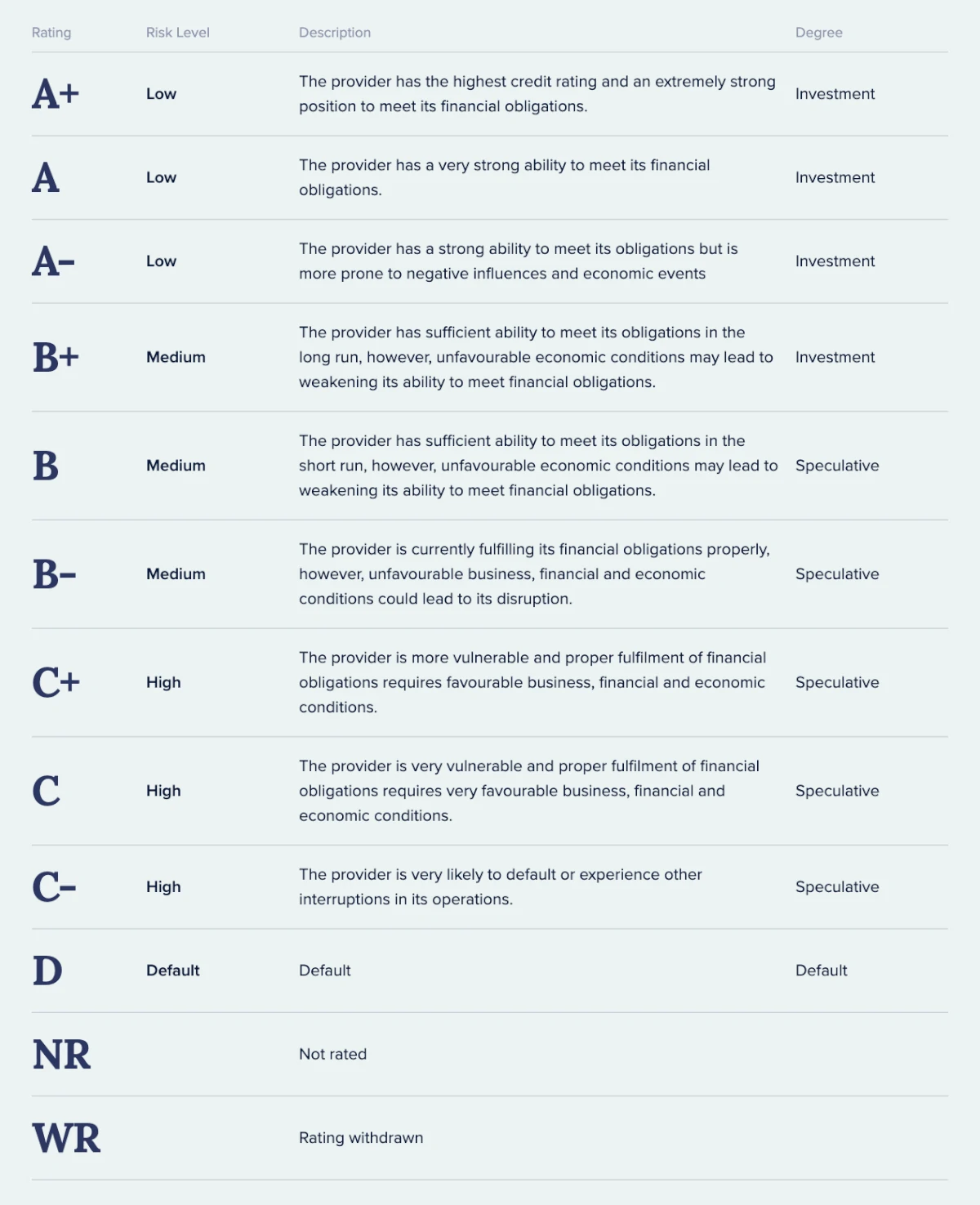

Bondster risk ratings

The loans on Bondster come with risk ratings. Keep in mind that the ratings are based on Bondster’s own risk rating methodology.

Two-factor authentication

Bondster offers two-factor authentication (2FA) to enhance account security. By using the Google Authenticator app, you receive unique, time-based passcodes that substantially reduce the risk of unauthorized access. Enabling 2FA is strongly recommended to help protect your investment funds and maintain peace of mind.

What is the return on Bondster?

Bondster’s average annual investment return is 11.90%. This places the platform in the mid-range compared to other P2P platforms in Europe, where typical advertised returns often range from around 10% to 15%. While Bondster’s headline figure is appealing, it also suggests taking on a moderate to higher risk profile.

The interest rates on Bondster ranges from 10% to 16%, which is relatively high in the sector. Higher returns typically correlate with higher risk, so it’s worth weighing potential gains against the challenges of late payments or defaults.

Bondster’s returns can be less stable than those of some lower-yield platforms, mainly because reliance on buyback guarantees and timely repayments can introduce variability in actual results. When loans remain unpaid or guarantees lapse, the effective yield can decline.

Time-limited welcome bonus

Readers of this Bondster review are eligible for a 1% cashback bonus on all investments for 90 days. To unlock this time-limited offer, new investors must sign up using the button below and invest at least €5. No Bondster promo code is required.

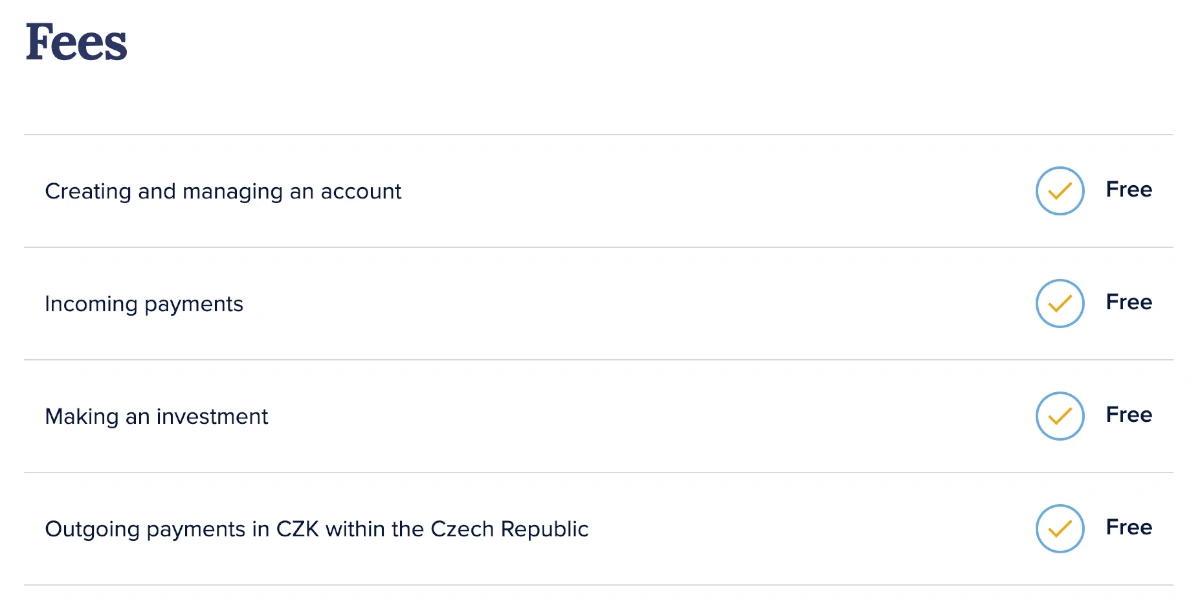

What are the fees on Bondster?

Bondster has no investment fees on the platform. Here is the fee overview from Bondster’s website:

Even though it seems like there are no fees, there is actually a 0.5% fee for selling loans on the secondary market.

Does Bondster withhold taxes?

Bondster does not withhold taxes from investors’ earnings. This makes it easier for you to handle your taxes compared to some regulated competitors, such as Mintos, NEO Finance, VIAINVEST, and TWINO, which do withhold a portion of your earnings for tax purposes.

Tax report

Bondster provides a tax report to simplify declaring your earnings to local authorities. To generate your tax statement, simply log in to your Bondster account, head to the transactions overview, and effortlessly download a statement for the chosen timeframe.

Who can invest on Bondster?

It is possible for both private individuals and companies to invest via the Bondster P2P platform.

Individuals

To create an account as an individual, you must meet the following requirements:

- Be a least 18 years old

- Have a bank account in the European Union

If you meet the above requirements, it is easy to get started at Bondster.

Companies

It is also possible for companies to invest via Bondster. After having clicked “register” on the website, simply select “legal entity” instead of “individual” in the signup form. This will give you a slightly different registration form. But from here, the user creation process is straightforward.

How to invest on Bondster?

Before you can start investing on Bondster, you must complete the following steps:

- Sign up on the Bondster website.

- Verify your identity.

- Complete the KYC questionnaire.

- Deposit funds into your account.

The entire registration process usually takes about 5-10 minutes, including signing up, verifying your identity, filling out any required questionnaires, and making your first deposit.

You can deposit money into your Bondster account using SEPA transfers. The minimum deposit is €0.01, and funds typically arrive within 1-3 business days. It is only possible to deposit funds in Euros (EUR) or Czech Crowns (CZK).

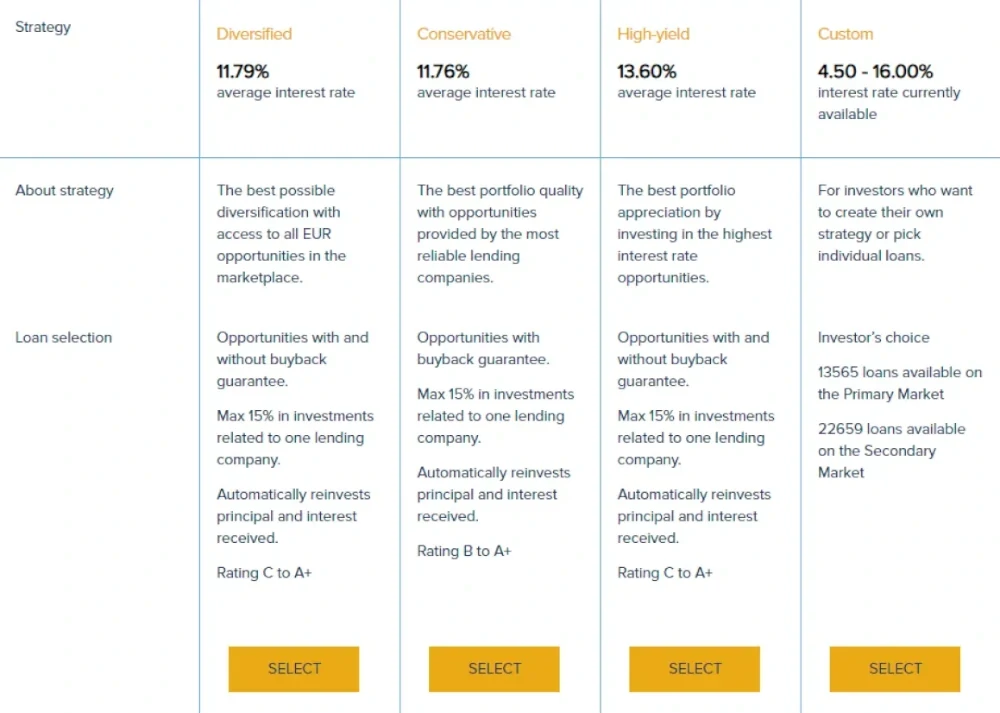

Once you have funded your account, you can start investing in P2P loans on the platform. Bondster allows you to invest manually by browsing available loans or automatically using a predefined or custom auto-invest strategy.

Bondster auto-invest

Bondster provides an auto-invest feature to automatically allocate funds into suitable loan investments based on each investor’s predefined criteria, saving time and simplifying the investment process.

The auto-invest tool enables you to configure key parameters, including portfolio size, maximum investment per loan, interest rate, loan term, loan type, loan status, countries, and loan originators. You can also automatically reinvest all returns.

Setting up a Bondster auto-invest strategy only takes 1 minute, and your funds should be invested within a few hours. If your auto-invest is not working, it is usually due to a lack of loans that meet your criteria. This can happen when your filters are too narrow or when no suitable loans are available.

How to withdraw money from Bondster?

You can withdraw your uninvested funds from Bondster at any time using the withdrawal section of your investor account. The minimum withdrawal amount is €0.01 and it usually takes 1-2 business days for your funds to arrive in your bank account.

Bondster does not charge any fees for withdrawing funds from your account, but your bank may charge fees for receiving international transfers.

To exit Bondster, you must first turn off all auto-invest strategies and sell any existing loans on the secondary market. If you hold non-performing loans, the platform must first recover the underlying debt before allowing withdrawals, which can negatively affect your liquidity.

Bondster secondary market

Bondster offers a secondary market for all its investments, enabling users to sell their holdings and exit the platform if needed. While sellers are charged a transaction fee of 0.5%, buyers can use the secondary market without any fees.

The time it takes to sell investments on the Bondster secondary market varies based on the price set by the seller and current market conditions. Sellers can list loans at their face value or add discounts or premiums to attract buyers. Each listing remains valid for up to 90 days before sellers need to relist.

Loans that are over 60 days late cannot be listed on the secondary market.

What are the best Bondster alternatives?

Some of the best alternatives to Bondster are Esketit, Lendermarket and Nibble Finance.

Conclusion of our Bondster review

Bondster is a moderately appealing P2P lending marketplace due to its competitive interest rates and user-friendly features. The platform sets itself apart from competitors by offering flexible diversification settings and strong backing from its parent company.

While Bondster offers a relatively high average return, a user-friendly auto-invest tool, and a secondary market that allows for additional liquidity, potential investors should be aware of its unregulated status, reports of questionable loan originators, and varying reliability of buyback guarantees.

Bondster might be worth it for investors who seek higher yields and can tolerate moderate to high risk in pursuit of strong returns. It is not be a good investment for risk-averse individuals who desire a fully regulated environment and more consistent buyback protections. If you prefer a regulated platform with a more reliable buyback guarantee, consider other P2P lending platforms.