EstateGuru review 2025

Read this EstateGuru review, and learn if the platform is for you.

EstateGuru

Pros

Cons

EstateGuru review summary:

EstateGuru is a real estate crowdfunding platform offering potential returns of around 10%. However, high default rates and limited communication raise concerns. While EstateGuru provides useful features like a secondary market and auto-invest, it is not worth it for risk-averse investors. If you seek reliability you may want to explore other real estate crowdfunding platforms.

It’s 100% free to open an account

Introduction to our EstateGuru review

This EstateGuru review introduces the platform, highlights its main features, and touches on its safety aspects. Remember, these are just our opinions and not financial advice. Use the navigation below to find what you need.

Learn about the following in our EstateGuru review:

- What is EstateGuru?

- What is the return on EstateGuru?

- Is it safe to invest on EstateGuru?

- Who can invest on EstateGuru?

- How to invest on EstateGuru?

- How to withdraw money from EstateGuru?

- What are the best EstateGuru alternatives?

- Conclusion of our EstateGuru review

What is EstateGuru?

EstateGuru is a real estate crowdfunding platform launched in 2014 and located in Tallinn, Estonia. It specializes in short-term, mortgage-backed loans and advertises an average net return of around 10%.

EstateGuru works by connecting investors with real estate project owners. Project owners benefit from faster and more cost-effective funding than traditional lending options, while investors can access a range of property-backed loans.

The platform has over 162,000 investors. They have collectively funded projects worth more than €865 million.

EstateGuru OÜ is regulated and holds a European Crowdfunding Service Provider license granted by the Estonian Financial Supervision Authority.

EstateGuru statistics:

| Launched: | 2014 |

| Investors: | 162,000 + |

| Interest rate: | 7 – 13 % |

| Loan period: | 9 – 24 months |

| Loan type: | Real estate |

| Loans funded: | € 865,000,000 + |

| Min. investment: | € 50 |

| Max. investment: | Unlimited |

EstateGuru management team

EstateGuru has a very experienced management team when it comes to real estate and finance. Many of the members had loads of experience in the field before joining EstateGuru, which is very positive.

The management is led by Marek Pärtel, co-founder and CEO of EstateGuru. He has been involved in the real estate industry since 2002 and has carried out development and investment projects in several European markets.

EstateGuru Trustpilot rating

Estateguru has received a TrustScore of 1.4/5 based on 1,235 reviews on Trustpilot. While some investors initially found the platform appealing for its real estate-backed loans and potential returns, many reviewers now report high default rates, limited communication, and frustration with added fees. Despite these criticisms, a few users have seen successful repayments and maintain hope that improved due diligence and transparency might help restore investor confidence.

What is the return on EstateGuru?

EstateGuru’s average annual investment return is 10.59%. This figure places the platform around the mid-range compared to the broader real estate crowdfunding market, which typically advertises returns between 6% and 15%.

The interest rates on EstateGuru ranges from 7% to 13%. While these rates may appear attractive, higher returns typically correlate with higher risk. Moreover, if available funds remain uninvested for extended periods (a phenomenon known as cash drag), the overall earnings can be diluted. EstateGuru’s performance has experienced fluctuations in some cases, indicating that the returns are not always entirely stable.

Time-limited welcome bonus

Readers of this EstateGuru review are eligible for a 0.5% cashback bonus on all investments for 90 days. To unlock this time-limited offer, new investors must sign up using the button below and invest at least €50. No EstateGuru promo code is required.

Does EstateGuru withhold taxes?

EstateGuru does not withhold taxes from investors’ earnings, allowing you to manage your tax obligations more directly. This approach differs from certain competitors like Crowdpear, Crowdestate, and Mintos, which withhold a portion of your earnings for tax purposes.

Tax report

EstateGuru provides a convenient tax report to help simplify filing your earnings with local authorities. You can easily download your income statement from your dashboard on the platform.

Is it safe to invest on EstateGuru?

EstateGuru is not considered one of the safest real estate crowdfunding platforms in Europe. Although the platform is transparent about loan performance, only 56.58% of the loans are current, while the rest are delayed or in recovery. This indicates a significantly higher level of risk for investors.

Although the EstateGuru’s average Loan-to-Value (LTV) ratio is 62.68%, indicating moderate leverage per project, it does not necessarily eliminate risk. Many Trustpilot reviewers have raised concerns about limited communication when loans are in recovery and have even referred to the platform as a scam.

EstateGuru OÜ is regulated and holds a European Crowdfunding Service Provider license granted by the Estonian Financial Supervision Authority. This regulated status suggests that it is a legit platform, though the risks associated with delayed or in-recovery loans should not be overlooked.

Two-factor authentication

EstateGuru offers two-factor authentication (2FA) to strengthen account security. This feature works with the Google Authenticator app, generating unique, time-based passcodes that protect investor funds from unauthorized access. Since hackers have targeted P2P lending platforms in the past, enabling 2FA is strongly recommended.

Who can invest on EstateGuru?

To be able to invest via EstateGuru, you must comply with the following requirements:

- Being at least 18 years old

- Have a bank account in EEA member states or Switzerland (Transferwise works for global investors)

- Fill in the appropriateness questionnaire

- Comply with KYC checks

If you meet the few requirements, you can start investing through EstateGuru.

How to invest on EstateGuru?

Before you can start investing on EstateGuru, you must complete the following steps:

- Sign up on the EstateGuru website.

- Verify your identity.

- Complete the KYC questionnaire.

- Deposit funds into your account.

The entire registration process usually takes about 5-10 minutes, including signing up, verifying your identity, filling out any required questionnaires, and making your first deposit.

You can deposit money into your EstateGuru account using SEPA transfers. The minimum deposit is €0.01, and funds typically arrive within 1-3 business days. It is only possible to deposit funds in Euros (EUR).

Once you have funded your account, you can start investing in real estate loans on the platform. EstateGuru allows you to invest manually by browsing available loans or automatically using an auto-invest strategy.

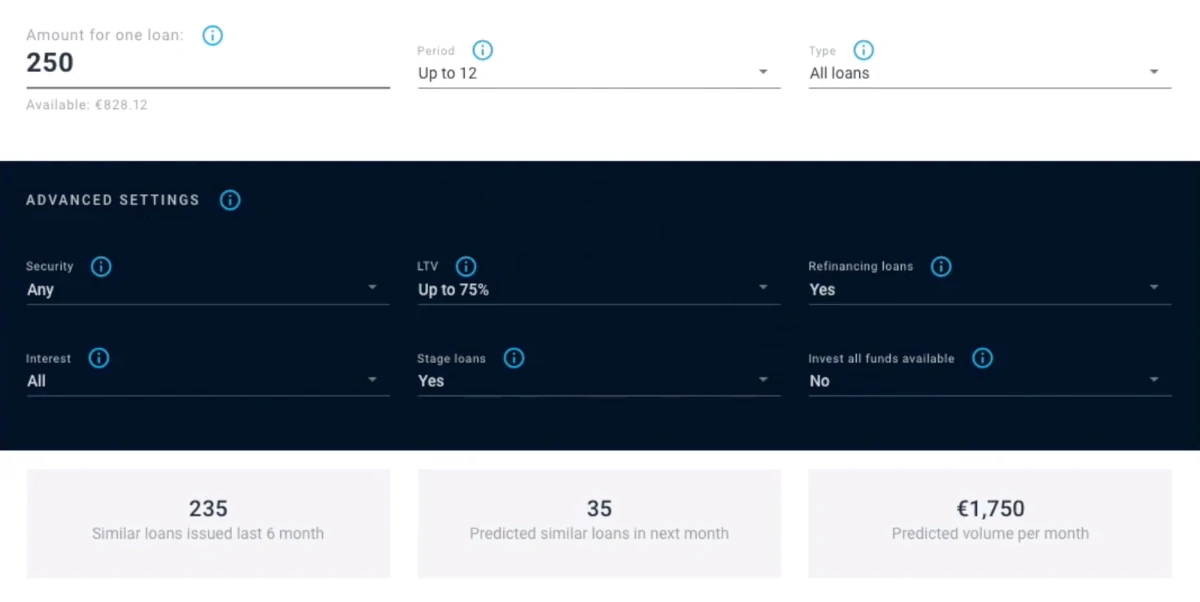

EstateGuru auto-invest

EstateGuru provides an auto-invest feature to automatically allocate funds into suitable loan investments based on each investor’s predefined criteria, saving time and simplifying the investment process.

The auto-invest tool enables you to configure key parameters, including maximum investment per loan, interest rate, loan term, loan type, and LTV. You can also automatically reinvest all returns.

Setting up a EstateGuru auto-invest strategy only takes 1 minute, and your funds should be invested within a few hours. If your auto-invest is not working, it is usually due to a lack of loans that meet your criteria. This can happen when your filters are too narrow or when no suitable loans are available.

How to withdraw money from EstateGuru?

You can withdraw your uninvested funds from EstateGuru at any time using the withdrawal section of your investor account. The minimum withdrawal amount is €0.01 and it usually takes 1-2 business days for your funds to arrive in your bank account.

EstateGuru charges a €3 service fee for withdrawing funds from your account, and your bank may also charge fees for receiving international transfers.

To exit EstateGuru, you must first turn off all auto-invest strategies and sell any existing loans on the secondary market. If you hold non-performing loans, the platform must first recover the underlying debt before allowing withdrawals, which can negatively affect your liquidity.

EstateGuru secondary market

EstateGuru offers a secondary market for all its investments, enabling investors to sell their loans at any time before maturity. While sellers are charged a transaction fee of 3%, buyers can use the secondary market without any fees.

The time it takes to sell investments on the EstateGuru secondary market varies based on the price set by the seller and current market conditions. Sellers can list loans at their face value or add discounts or premiums to attract buyers. Each listing remains valid for up to 14 days before sellers need to relist.

Loans bought on the primary market can be sold immediately on the secondary market, while those purchased on the secondary market must be held for 30 days before resale.

EstateGuru’s secondary market is expensive compared to other real estate crowdfunding platforms. Investors who actively use secondary markets may want to consider more affordable alternatives, such as PROFITUS or Crowdpear.

What are the best EstateGuru alternatives?

Some of the best alternatives to EstateGuru are PROFITUS, Indemo, Brickstarter, Letsinvest, Fintown and Lemox. These real estate crowdfunding platforms each provide distinct areas of focus, offering a range of unique projects that set them apart from EstateGuru.

Conclusion of our EstateGuru review

EstateGuru is a questionable real estate crowdfunding platform due to its high default rates and limited communication.

While EstateGuru offers a convenient secondary market, auto-invest functionality, and no investment fees, the low rating on Trustpilot, a €1 withdrawal fee, and a 3% selling fee on the secondary market highlight significant drawbacks.

EstateGuru might appeal to investors seeking short-term real estate loans and moderate yields. It is not a good investment for risk-averse individuals who require lower default risks, clearer communication, and more reliable performance. If you seek a more reliable platform, check out these real estate crowdfunding platforms instead.