Limedot review 2024

In this Limedot review, you will get an extensive breakdown of the P2P lending platform’s features, pros, and cons. You can see a summary just below or read our full analysis to help you decide if the Limedot platform is the right fit for you.

Limedot

Pros

Cons

Limedot review summary:

Limedot is a new P2P lending platform focusing on Southeast Asian loans, offering an average 13.50% annual return. It stands out for its transparency about loan originators and safety features like a 10% skin in the game requirement and buyback obligation. The platform is user-friendly with features like auto-invest and a secondary market. The experienced team behind Limedot adds to the platform’s trustworthiness. Looking at the downsides, Limedot lags diversification options and have a short track record.

It’s 100% free to open an account

Introduction to our Limedot review

This Limedot review provides an overview of the P2P lending platform, focusing on its features, fees, safety, user experience, and more. It aims to help investors make an informed decision about using the platform.

Please note that the content is our opinion and not financial advice. The Limedot review covers various aspects, and readers can click on the links for specific topics of interest.

By the end, investors should have a better understanding of whether Limedot is suitable for their investment needs.

Learn about the following in our Limedot review:

- What is Limedot?

- Main features

- What rate of return can you expect?

- Who can invest via Limedot?

- How safe is Limedot?

- Best Limedot alternatives

- Conclusion of our Limedot review

What is Limedot?

Limedot is a P2P lending platform that allows investors to invest in business loans from loan originators in Vietnam. It was launched in 2022 and is incorporated in Ireland. The platform was founded by Marek Krakops.

Limedot works as a facilitator that connects lenders with investors. The platform differentiates itself from other platforms by mainly having a focus on Asian markets. On the platform, investors gain access to loans from Moneyveo Asia and Alocash. Both loan originators are focused on long-term business loans.

All loans on the platform are protected by a buyback guarantee the average return on Limedot is currently 13.50%.

Since its inception in 2022, Limedot has successfully expanded its investor base to include more than 400 investors.

With a minimum investment of €10, you can start investing on limedot.eu.

Limedot statistics:

| Launched: | 2022 |

| Investors: | 400 + |

| Interest rate: | 12 – 15 % |

| Loan period: | 1 – 2 years |

| Loan type: | Business |

| Loans funded: | Unknown |

| Min. investment: | € 10 |

| Max. investment: | Unlimited |

Limedot FAQ:

Limedot Trustpilot reviews:

Limedot is a young P2P lending platform without Trustpilot reviews.

Main features

In the following part of our Limedot review, you can learn about the main features of the platform, and why they are important for you as an investor.

1. Limedot buyback guarantee

Limedot provides an extra safety feature for investors called a buyback guarantee. This guarantee protects investors if the borrower doesn’t pay for over 60 days. In this case, the company that gave the loan has to buy it back. This includes the initial amount of the loan and any interest. This gives more protection to the investors.

However, the value of this guarantee depends on the loan originator’s ability to pay it. If they can’t pay, the guarantee won’t help the investors. You should never depend only on a buyback guarantee.

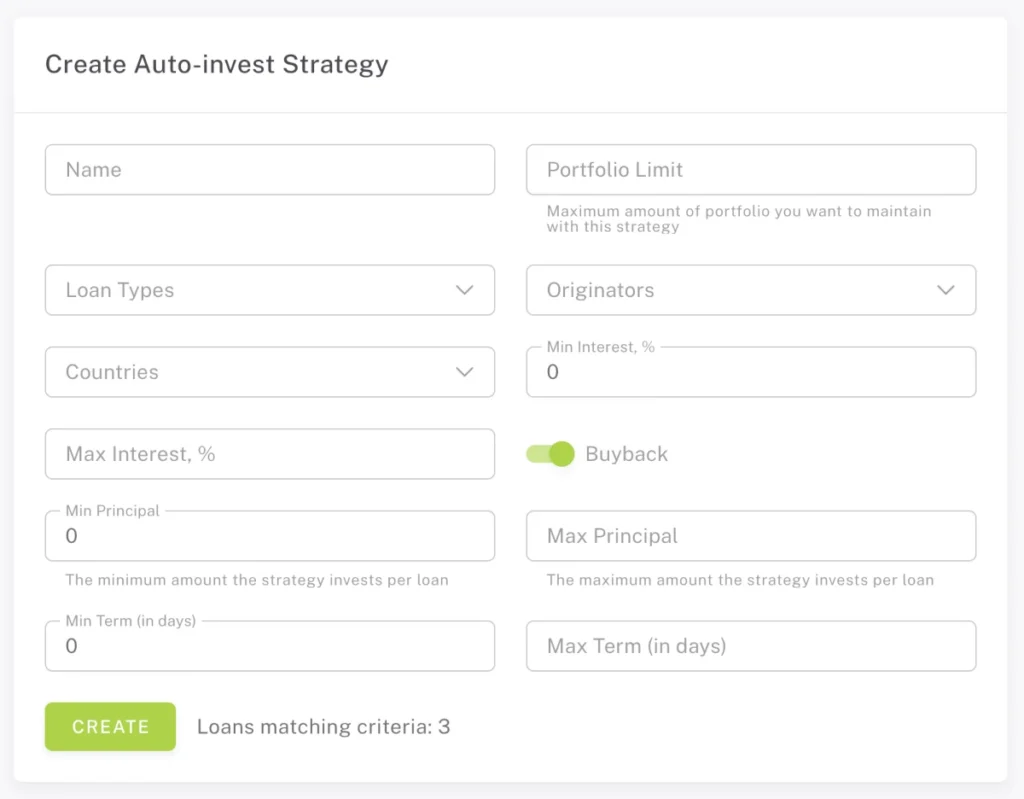

2. Limedot auto-invest

Limedot offers an auto-invest tool that makes it possible to automate investing on the platform. Auto-invest is easy to set up on the platform and you can access it in the user dashboard.

When you use the auto-invest tool, you first set your investment criteria. This includes the amount of money you want to invest, the desired interest rate range, the loan term, and other parameters that match your investment strategy. You have a lot of different options to choose from. When you set up the tool, you can see how many loans are matching your criteria.

Based on the preferences you’ve set, the auto-invest tool automatically allocates your funds to loans that meet your criteria. This means that when a loan that matches your settings becomes available, the system automatically invests a specified amount of your funds into it.

Once you’ve set up your auto-investments, the process runs automatically. This is ideal for investors who prefer a more passive approach to their P2P investments, saving time and effort that would otherwise be spent on manual selection and investment.

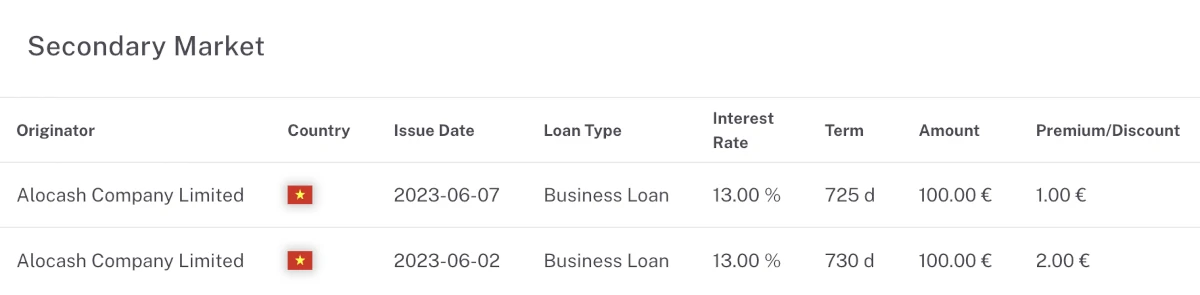

3. Limedot secondary market

The Limedot secondary market is a feature on Limedot that allows investors to buy and sell loans among themselves. This feature is particularly useful for providing liquidity in P2P lending, which typically locks funds into loans for their duration.

This secondary market feature adds significant flexibility to Limedot, as it allows investors to adjust their portfolios without being bound to the original loan term.

However, users need to understand that the ability to sell loans depends on the demand from other investors and the pricing strategy they choose.

You should be aware that the secondary market on Limedot is not that active compared to other platforms like Mintos due to the size of the platform. This means that it can take longer to sell loans than on other platforms.

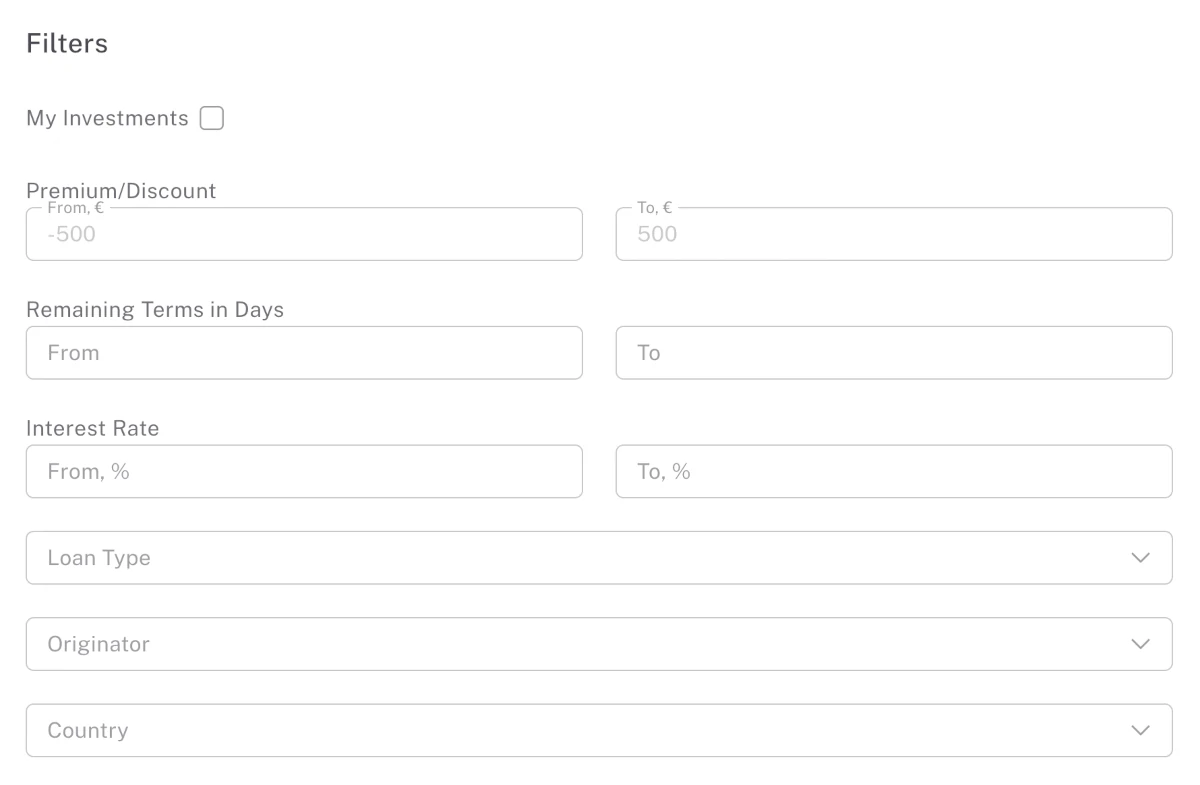

When using the Limedot secondary market, you can use the following filters:

What rate of return can you expect?

The average annual return on Limedot is 13.50%. This means that you can reasonably expect a return in that range. However, your actual return depends on how you choose to invest on the platform.

The return on Limedot is similar to what you can find on other platforms.

Who can invest via Limedot?

To invest via Limedot as a private person, you must meet the following requirements:

- Be a least 18 years old

- Live in the EEA

If you match the aforementioned qualifications, getting started with Limedot is simple. Simply follow the steps below, and you should be up and running in no time:

- Sign up at https://limedot.eu/

- Add funds to your account

- Invest in loans with auto-invest

Available countries

Limedot is available to investors in the European Economic Area (European Union, Iceland, Liechtenstein, and Norway), Switzerland, and the United Kingdom.

If you are looking for another platform that is available outside of Europe, you should instead check out Debitum.

Do you meet the requirements to sign up as an investor at Limedot? Then press the button below to get to their website. From here you can quickly create a free account and get started investing:

How safe is Limedot?

Security is one of the most crucial factors to consider while investing money online through peer-to-peer lending websites. As a result, we have examined the platform’s security in our Limedot review.

The two areas that we examined are the safety of the investments and the company’s stability.

How safe are the investments?

The first thing we looked into when creating this Limedot review, is how secure the investments are.

Loan originator risk

All loans on Limedot come from external lending companies as the platform only acts as a facilitator of loans. Here is an overview of the lending companies in Limedot:

- Moneyveo Asia

- Alocash

Each of these loan originators can pose a risk to investors. If a loan originator encounters financial challenges it can impact their ability to fulfill the buyback obligation.

Limedot mitigates this risk through several measures. First and foremost, the CEO and founder’s extensive 15 years of expertise and extensive industry experience are used to conduct a thorough due diligence and onboarding process for Loan Originators.

The loan originators on Limedot adhere to the “skin in the game” principle, which requires them to retain a minimum of 10% of each loan in their portfolio.

Loan originators must also provide the lender portfolio pledge to secure its obligations in case the lender provides investment to the investor through the assignment agreement. If the loan originator goes out of business, investors may still retain ownership of their claim rights and have a chance to recover their funds, depending on the specific loan structure in place.

There are only a few loan originators on Limedot, which can make it hard to achieve proper diversification and lower your loan originator risk. If this is a concern to you, it can be a good idea to also use other platforms together with Limedot.

Buyback obligation

On Limedot, the loans are covered by a buyback obligation. This means that your investments will be bought back if the borrower doesn’t repay before the loan is 60 days overdue.

As previously mentioned in this Limedot review, a buyback obligation is only as solid as the one behind it. You should never rely solely on the buyback guarantee when you invest via Limedot.

How solid is the company?

It’s unclear from the given information if Limedot is currently profitable or how well it is performing financially. While it’s true that setting up a P2P platform can initially be costly, a prolonged lack of profitability could be risky for investors.

If Limedot goes bust, necessary measures will be taken to transfer the servicing of all concluded assignment agreements and investments to a suitable administrator. This means that you will not lose your investments and the administrator can assist in recovering your outstanding payments.

Best Limedot alternatives

Are you unsure if Limedot is the right platform for you after reading this Limedot review?

With hundreds of P2P platforms available, it can be difficult to determine whether you have found the best platform or if you should explore other Limedot alternatives.

The main categories for P2P platforms include consumer loans, real estate, and business loans.

Here are the best Limedot alternatives right now:

There are several reasons why you should consider a Limedot alternative.

First and foremost, you may find that Limedot does not meet your investment needs. Every P2P investor has different requirements when it comes to lending platforms. Therefore, you must understand your main investment criteria and find a platform that aligns with them.

Additionally, it can be a good idea to diversify your investments across multiple platforms, such as the ones mentioned above, to reduce overall platform risk.

Conclusion of our Limedot review

Limedot is a new and promising P2P lending platform that offers investors an average annual return of 13.50%. Compared to other platforms this return is quite competitive. Limedot differentiates itself from other platforms in the platform’s focus on funding loans in the Southeast Asian market.

Limedot is very transparent about loan originators, which is a huge plus. Currently, you can invest in loans from Alocash and Moneyveo Asia. Limedot has a “skin in the game” requirement of 10% and a buyback obligation on loans which adds to the safety of the platform.

Limedot is user-friendly and has all the expected features like an auto-invest function and a secondary market for making an early exit. It is straight forward creating an account and identity verification was surprisingly fast at around 2 minutes.

Limedot is led by an experienced team with significant experience in finance which adds trust to this otherwise new platform.

Overall, Limedot is a very good P2P lending platform for investing in loans from Asia.

Do you want to sign up after reading this Limedot review? Click the button below to visit the website where you can become an investor: